Chart of the Week: Short Stack

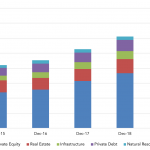

Of the $6.7 trillion of private capital assets under management in the US, only $800 billion is private credit.

Of the $6.7 trillion of private capital assets under management in the US, only $800 billion is private credit.

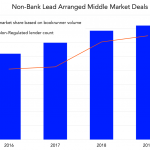

Middle market syndicated loans are increasingly led by direct lenders, taking share from banks.

2019 leveraged loan volume was off 35%; the second straight decline since the 2017 peak.

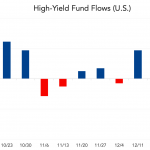

Last year was a strong one for junk bond funds, as $19 billion entered mutual funds.

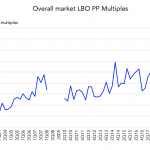

Purchase price multiples for all leveraged buyouts have steadily risen since the Great Recession.

Secondary liquid loan prices are lifting as CLO managers use conserved cash to buy higher yielding (B2/B3) assets.

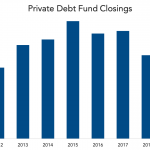

The number of private debt funds closed through June 30 was significantly off last year’s pace.

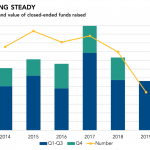

Overall fundraising for private debt strategies peaked in 2017, but is poised for another solid year in 2019.

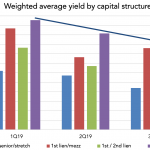

First-lien/mezz is the costliest capital structure for sponsors; unitranche is coming down.

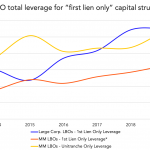

Leverage for middle market unitranches has matched first-lien large cap leverage.