Chart of the Week: Volume Game

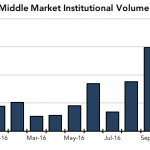

Month over month, both October and November have seen improvements over last year in middle market sponsored loan activity.

Month over month, both October and November have seen improvements over last year in middle market sponsored loan activity.

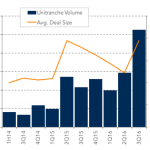

3Q 2016 was the most active quarter in the past several years for unitranche financings, as middle market sponsors increasingly access the non-bank market.

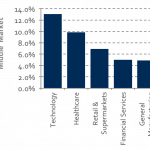

Five sectors comprise 60% of all middle market institutional loans.

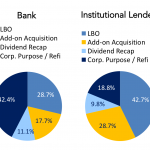

Middle market borrowers look to banks for refinancings; for buyouts and add-ons, almost twice as many seek institutional lenders.

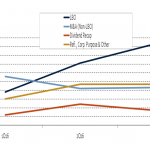

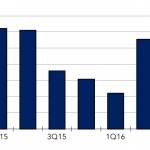

Middle market LBO volume was up 43% for the third quarter, far outpacing the number of add-ons, dividend recaps, and refinancings.

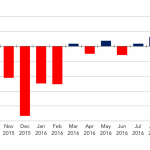

Add-on volume for the overall market rebounded sharply during 2Q 2016 from the first quarter, though slowed last quarter.

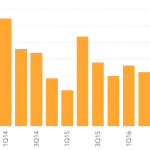

Sponsored acquisition volume for platform companies has averaged less than $2 billion for past five quarters

So far in October, middle market loan activity is tracking for its fourth consecutive month-over-month improvement.

Driven by a benign credit environment and favorable relative value dynamics, $2.5 billion has flowed into retail loan funds.

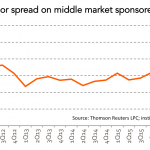

Spreads for middle market sponsored loans have generally remained range-bound around L+500 for the past four years.