As we prepared this past weekend to escape the 95°F cauldron of Manhattan for the relief of the 98°F oven in the Outer Banks, our thoughts turned to which industries have proven to be the hottest so far this year.

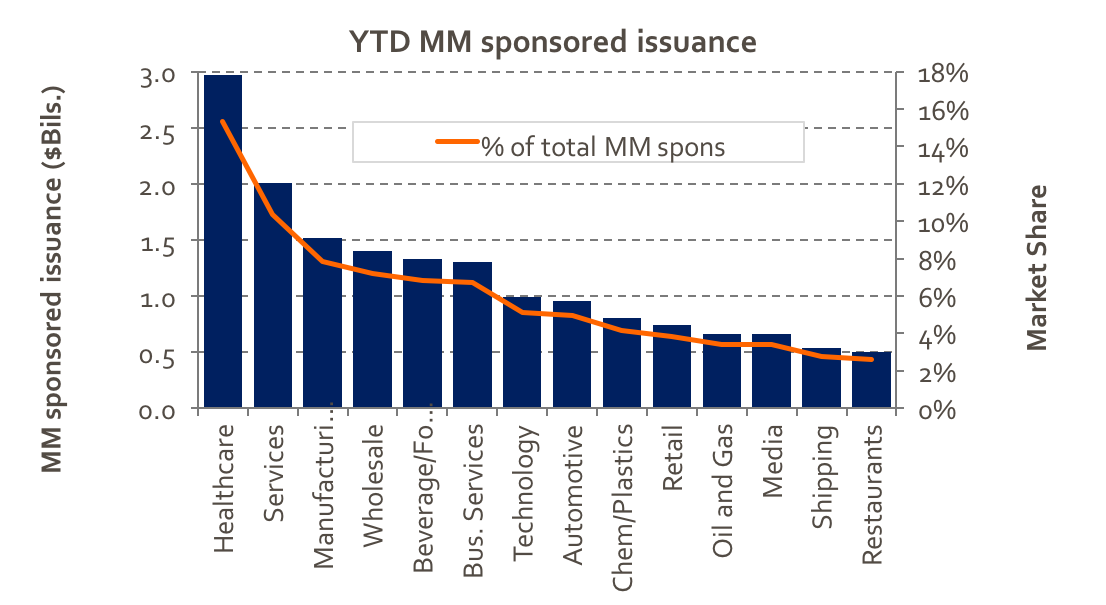

In terms of new issues for middle market sponsored transactions, healthcare has been the most active both this year and 2015, according to Thomson Reuters. As our Chart of the Week illustrates, private equity sponsors recorded about $3 billion in deal activity in that sector through this month. That tracks 2015's full year tally of $6.4 billion.

Our experience has confirmed this trend, with healthcare services, technology, and devices topping the most active sub-sectors in the space.

The reasons for this are several. Private equity sponsors with successful track records in healthcare have well-established views by now on matters such as reimbursement risk, electronic medical records, and insurance reform.

There is also the fact that healthcare spending continues to be the largest expenditure as a share of US GDP at 17%. This is followed by education and defense that weigh in at 6% and 3.5%, respectively.

Finally, debt providers have noted that healthcare has been one of the better performing sectors both during and after the credit crisis. Specialties such as physician outplacement, long-term care, and urgent care clinics continue to see high valuations.

Healthcare M&A activity in the middle market has been the second busiest area, with almost $2 billion of deal flow so far this year; second only to technology at just over $2.1 billion, per Thomson.

Speaking of which, technology-oriented businesses represented over $3.5 billion in new money mid-cap financings so far this year. That topped healthcare, manufacturing, and business services. Tech-enabled software, for example, has been particularly active as companies have worked to cut costs in the face of tepid growth.

Tech companies have also seen senior leverage rise to almost 4.5x through June 30. Healthcare and services borrowers are a distant second with senior debt to ebitda less than 4.0x. On average total leverage has eased below 5.0 x for all industries.

At the other end of the spectrum, out-of-favor sectors such as oil and gas, media, shipping, and restaurants are at the bottom in terms of sponsored issuance. This coincides with the worst categories in terms of defaults in overall leveraged loans - metals/mining, oil/gas, and printing/publishing.

It will thus be challenging to see how lenders manage some $4.75 billion of maturities that come due in the energy space during the final quarter of this year.

From the Editor: Beginning next week, The Lead Left will be on its annual August break and will return the week of September 5.

|

|

|

|

This week we chat with Jason Kelly, New York bureau chief, Bloomberg. Jason has been with Bloomberg since 2002. He is the author of

The Lead Left: Jason, your new book, Sweat Equity,

focuses on endurance sports and the fitness industry from the entrepreneur's perspective. What was the inspiration for this project?

Jason Kelly: It was both personal and professional. I've been running marathons since 1999, I started looking at how dollars were being spent. Running is simple, not a complicated sport. You basically have shoes and clothes. I realized I was spending a lot on not just those basic items, but also the cost of races, your travel, your food, and so on. And I was spending a lot!

The original idea was exploring people's personal spending habits. I looked around at people like me, who were running, doing yoga, triathlons, or cycling. As a business journalist, I've learned about following the money. So I focused on businesses I had noticed in the race and events space, as well as the boutique fitness boom. That's exploded in the last 5-6 years. I spoke to a lot of private equity partners and bankers in the space. Those guys show up when there are dollars to be made. I knew then I was onto something.

TLL: So how did you choose the stories in this book?

JK: I'm always looking for characters and there are a lot in and around this business. Whether it was Barry Jay of Barry's Boot Camp or Mary Wittenberg, formerly of New York Road Runners and now Virgin Sport. I wanted to focus on passionate people with great stories to tell. My business is mixing money with good stories.

"Millennials have demonstrated a willingness to spend money on experiences instead of 'stuff'."

TLL: Why now? Is it technology, the market, the focus on health? What trends have you seen?

JK: There are number of things colliding -- general awareness around healthier lifestyles, technology and some demographic and generational shifts. And once it gets going, it's hard to turn back the tide. Any meaningful experience with feeling healthy makes it hard to go back. People discovered that exercise makes them feel good. It keeps them coming back. Also, there's a deep sense of community building with these brands.

Technology plays a couple significant roles. Wearable technologies like Fitbit and the Apple Watch give us access to data about bodies and our workouts. Also, social media, whether Twitter or Instagram, plays a big part because we're able to show off a bit, to see what other people doing. And then there's an interesting aspect to technology where we're actually rejecting how much we rely on it. I think group fitness is a reaction to the superficiality of social media. Exercising together evokes something of a primal reaction -- there's something appealing about being together, sweating.

TLL: Is it a generational thing?

JK: Millennials represent a healthier generation. They grew up more fit, so it feels more natural to them, more than those of us who are 40 years or older. This is especially true of the social aspect of exercise. People in their 40s are more likely to pursue more solitary exercise like running. For millennials, it's very much of a group and social activity. And millennials have demonstrated a willingness to spend money on experiences instead of "stuff."

TLL: What are some of the long-term trends that you noticed?

JK: Women are primary drivers of this trend. Title IX was critical because it institutionally leveled the playing field, opening opportunities for girls to play sports from a young age. Starting in the 1980s, girls were able to experience sports through their entire educational experience. And once they graduate from college, they're not just going to give that up. Then you factor in that women tend to be responsible for household spending -- not just for themselves, but for families. They make the decisions around food, travel, and so forth. And now many are doing that with a healthier lens.

TLL: Jason, you have written extensively about private equity. What is their entry point into health and well-being?

JK: It's a relatively small universe of private equity firms who have gone deep or specialized in health and wellness. Firms such as L Catterton, North Castle, and Falconhead are a few examples. Amid the bigger firms, one of the more notable deals was TPG and Leonard Green's acquisition of Lifetime Fitness.

Also, with a number of bankers' help, I infiltrated into middle market and large cap firms, focusing on their sale/merger processes. It's still early days in the sector. It's still a nascent market. A good example is what I've seen with M&A activity around Equinox. Understanding the real estate piece associated with that company, their relationship with SoulCycle, and their creating their own line of hotels.

TLL: How does one distinguish between a fad and real trend in this industry?

JK: That's hard to calculate. Otherwise I'd be investing rather than writing! Smart investors are trying to make bets with exposure to mega-trends in health and wellness. These are intact. You and I in five years, for example, aren't going to say, "Let's go have a smoke."

Running is here to stay. Yoga has been around a couple thousand years. But spinning versus barre versus Pilates - who knows? It's hard to imagine 10 years from now, will we have 10 different indoor cycling competitors who are wildly successful? Or barre studios? Each have their distinctive personalities. That makes it very hard for investors.

To be continued the week of Sept 5

Contact: Jason Kelly

|

|

|

|

Vertical Drop

More new middle market sponsored deals have been in healthcare this year than any other sector.

Sources: Thomson Reuters LPC

|

|

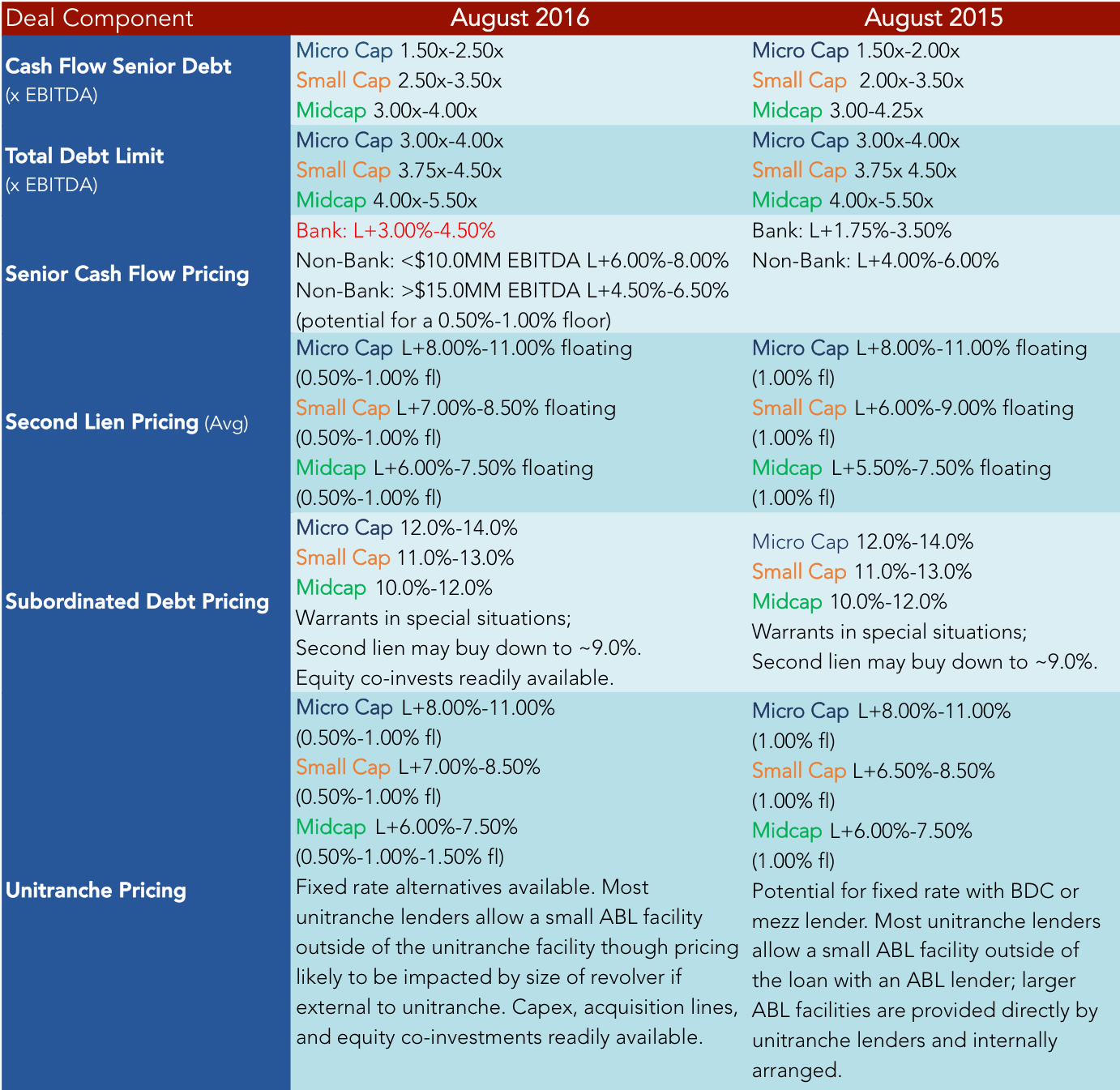

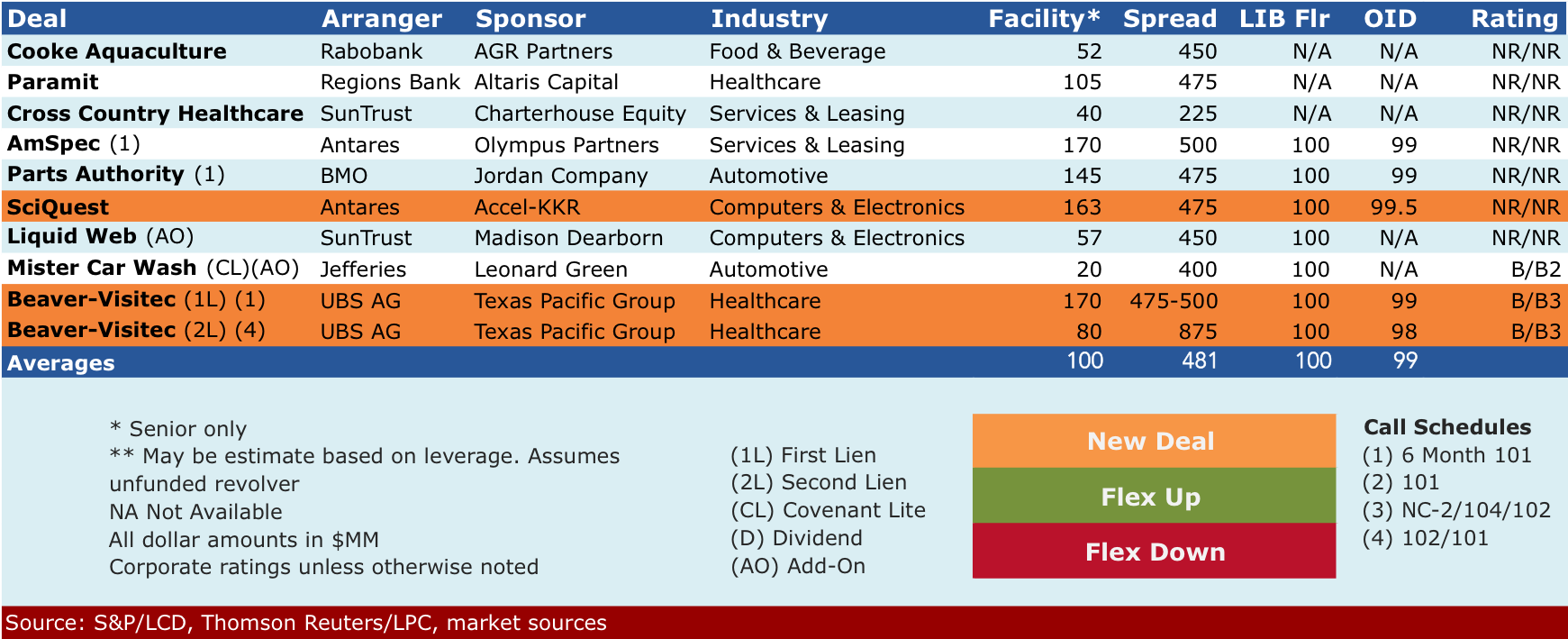

MIDDLE MARKET DEAL TERMS AT A GLANCE

|

|

LEVERAGE LOAN INSIGHT & ANALYSIS

|

Provided by:

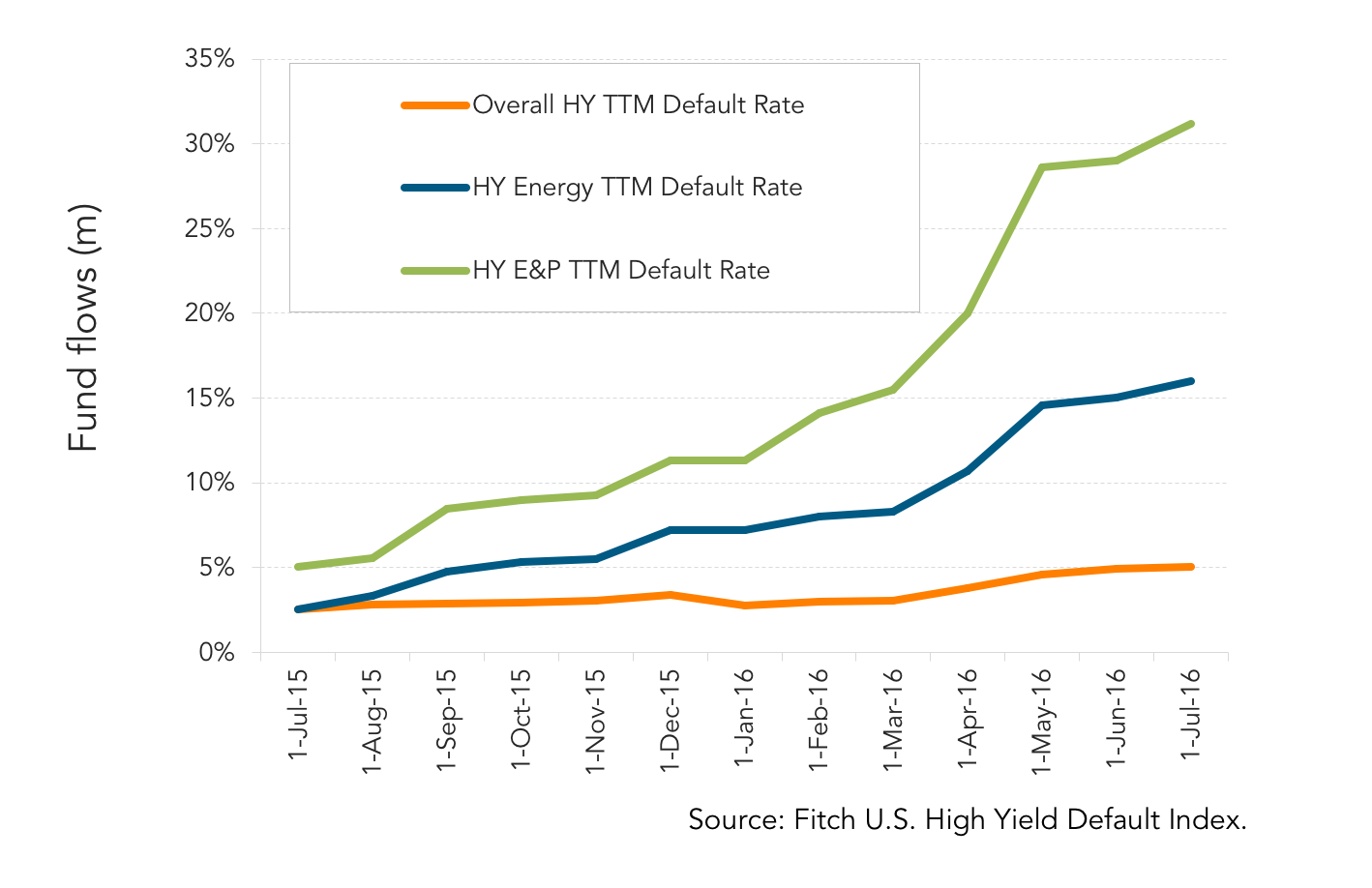

HY E&P Trailing 12-month default rate surpasses 31%

There was $5.2 billion of U.S. high yield bond default volume in July, pushing the trailing 12-month (TTM) rate to 5.1% from 4.9% at the end of June, according to Fitch Ratings. Halcon Resources Corp.'s long-awaited bankruptcy comprised nearly half of the July default total. The E&P company completed three distressed debt exchanges (DDE) in 2015 before filing on July 27. The market registered $39.9 billion of defaults over the past four months, with the energy sector comprising 67% of the total, led by Linn Energy LLC, SandRidge Energy Inc. and Energy XXI Ltd. Energy makes up $258 billion, or 17%, of the outstanding universe. Meanwhile, TTM energy defaults were $45.5 billion and 60% of the $55.4 billion YTD overall total. The July energy TTM default rate reached 16% while the E&P subsector rate climbed to 31.2%. Bankruptcies compose the majority of the sector's volume; however, there have been more DDEs done this year in number. Nearly half the names on Fitch's Bonds of Concern table are from the energy sector, with several candidates likely defaulting before the end of the year. Fitch Ratings expects the energy default rate to reach 20% during the year before settling at 16%-18% by year end.

|

|

THE PULSE OF PRIVATE EQUITY

|

Provided by:

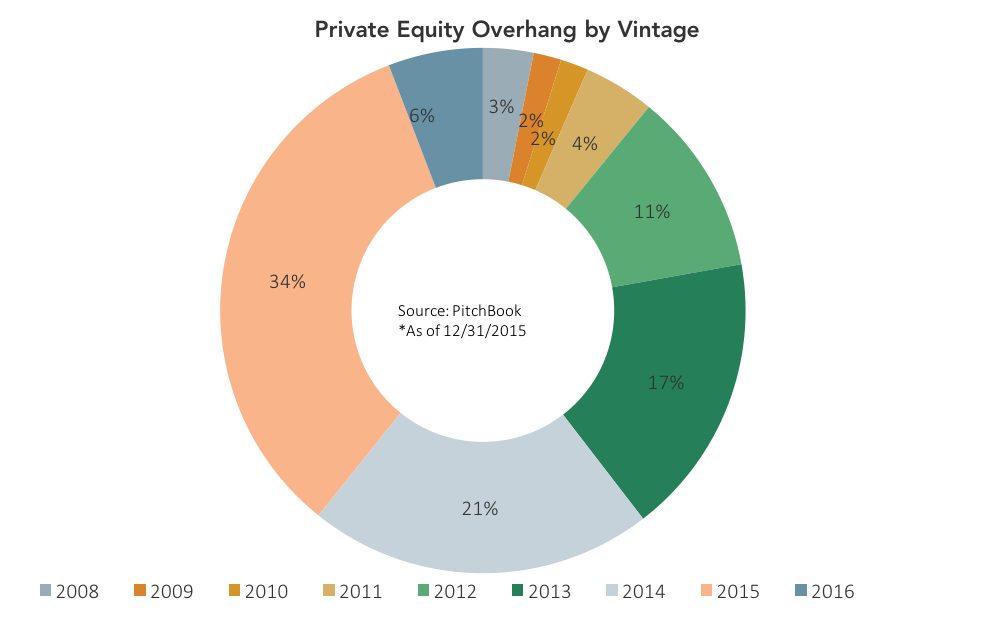

What does PE's capital overhang portend?

Through the end of 2015, the private equity industry in North America and Europe had an overhang of no less than $749.4 billion. A plurality of that is concentrated in funds of the 2015 vintage, with a majority-55%-in funds closed in the past two years (funds return data is overall through the end of 2015, with 2016 numbers from vehicles that have begun reporting yet have not fully closed). With such proportionate recency in mind, it's clear that PE investors have more than enough capital to fuel typical investment cycles for some time. For the midterm, the heft of capital in 2012-2013 vintages will continue to contribute to the upward pressure on valuations for worthwhile targets currently in the market. Both PE buyers and company sellers know that there is more than enough capital in funds to pay up for the right prospects, so even as dealmaking activity has softened overall as investors have grown more cautious, when they do enter the running, things can grow inflated rather quickly. This state of affairs shall persist for some time as the buyout cycle winds slowly down. With such a hoard of youthful dry powder, many PE funds are prepared for the onset of the next investment cycle, however, which will continue to see further deployment of niche strategies designed for a high-priced environment of varying quality, such as secondaries, lower-middle-market rollups and more.

☞ Read PitchBook's 2Q 2016 M&A Report here.

|

Provided by:

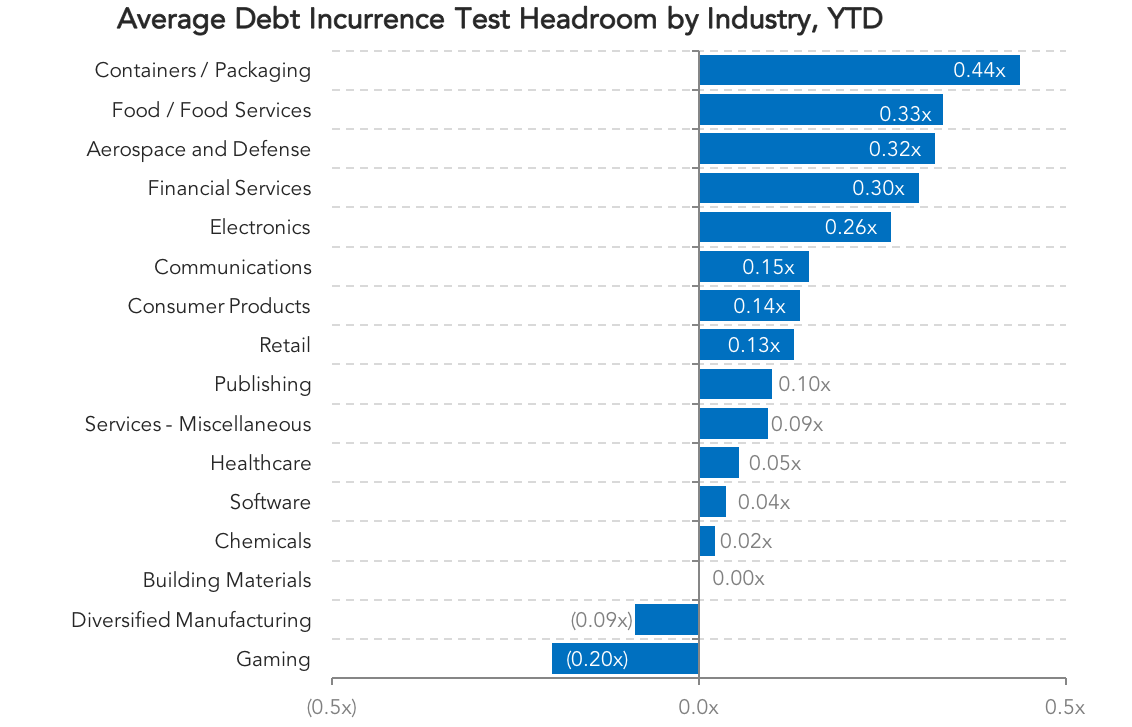

Average Debt Incurrence Test Headroom

|

|

|

|

PRIVATE DEBT INTELLIGENCE

|

MARKIT RECAP

|

|

Provided by:

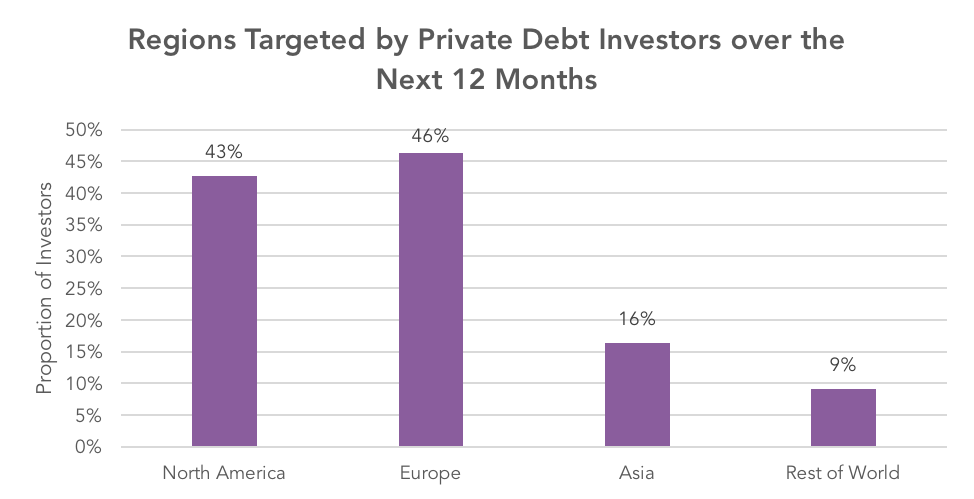

Private Debt Investors Target Europe

Despite recent lacklustre fundraising activity, the private debt industry continues to attract investors, due to the uncorrelated returns and regular income stream offered by the asset class. Ninety-four percent of private debt investors expect the size of the industry to increase over the next five years, with over a quarter (27%) predicting substantial progress.

In the midst of such expectations, Europe is emerging as the primary region for growth in the fundraising market, and the latest Preqin research finds that a greater proportion of private debt investors are now targeting Europe than North America. Forty-three percent of investors tracked by Preqin plan to target North America-focused funds over the next 12 months, in what has traditionally been the largest alternative lending market. However, Europe-focused funds are being targeted by 46% of investors over the next 12 months, as more LPs view the region as offering the best opportunities for return on their investment.

These latest figures reinforce Preqin's findings from a survey held December 2015, when investors stated that they were planning on committing more capital to Europe-focused than North America-focused funds for the first time in the history of the asset class. At the same time, there is mounting evidence that investors are starting to look even further afield to less congested markets. Asia in particular is beginning to attract the attention of investors, with 16% of investors looking to invest in the region. A further 9% of investors are intending to invest outside of the three regions and are targeting the as-yet fledgling private debt markets in other parts of the world.

This diversification of appetite among private debt investors bodes well for the long-term growth of the asset class. While North America-focused managers may no longer have the same primacy that they have previously enjoyed, there is no lack of appetite for the region; but as the private debt market continues to grow, we can expect regions like Europe and Asia to become an ever-more common part of investors' allocation plans.

Contact: William Clarke

|

Provided by:

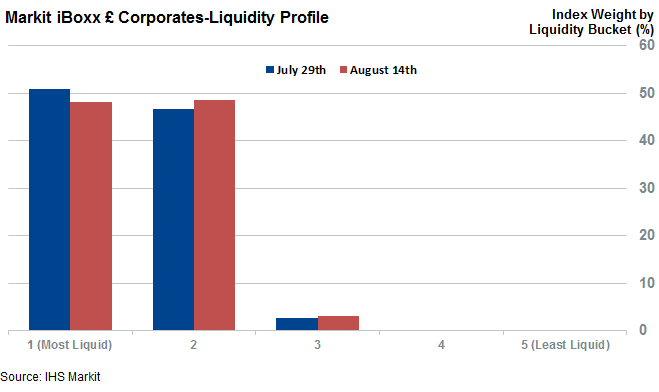

The Bank of England's (BoE) revamped quantitative easing (QE) program hit an early snag last week when the central bank failed to source enough gilts on just the second day of purchases. This early setback has caused some to question the impact of the bank's actions on the corporate bond market, and whether the bank would be able to source its targeted £10bn of investment grade corporate bonds without causing major liquidity disruptions when purchases start in September. While it's still early to draw definite conclusions about the program's impact on the asset class, there are few signs of a drying up in sterling denominated investment grade bond liquidity, as the asset class's liquidity profile has remained relatively unmoved in the two weeks since the program was unveiled.

The weighted average Markit liquidity score across the 677 bonds which make up the Markit iBoxx £ Corporates stood at 1.5 as of latest count with 96% of the index by weight scoring in the two most liquid buckets. The average liquidity score, which takes into account elements such as cost to trade bonds and the number of dealers willing to make a market for the individual bonds, has remained flat compared to the levels seen at the end of July; suggesting that QE hasn't radically impacted UK corporate bond liquidity.

The cost required to trade in and out of sterling corporate bonds has also remained unchanged, as the bid ask yield spread seen across the index has remained flat at 14bps over the last two weeks. Interestingly, financials' bonds, which are largely exempt from the QE program, are benefiting from lower trading costs as their average bid ask yield has fallen by 0.8bps at the end of July to 16.4bps.

The steady liquidity profile of UK corporate bonds is also underpinned by the fact that the number of dealers willing to make a market on the asset class has remained relatively unchanged in the last two weeks. An average of 5.7 quotes has been seen across the index's constituents over the last ten days compared to 5.9 in the ten closing days of July.

But unlike the bid ask yield, the number of dealers making a quote across financials bonds has shown signs of tapering in the ten days since corporate QE was announced. On average, bonds issued by financial firms have seen the number of dealers quoting fall from 5.8 to 5.2. This number is driven in part by the fact that the number of financials bonds which have received more than five daily quotes over the last ten trading days has fallen from 170 to 144. Non-financials bonds have seen the opposite, with 272 of the index's constituents now seeing more than five quotes, up from 263 at the end of July.

Although the falling number of quotes seen in financials' bonds hasn't impacted their trading cost, this trend is definitely worth monitoring given that the BoE's program will mostly focus on non-financials' bonds - which could make financials less attractive in the absence of a guaranteed buyer.

|

|

|

SELECT DEALS IN THE MARKET

|

|

This publication is a service to our clients and friends. It is designed only to give general information on the market developments actually covered. It is not intended to be a comprehensive summary of recent developments or to suggest parameters for any prospective financing opportunity.

|

|

|

|

|