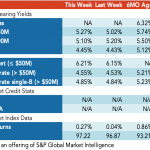

Loan Stats at a Glance – 5/17/2021

Contact: Marina Lukatskymarina.lukatsky@spglobal.com

Contact: Marina Lukatskymarina.lukatsky@spglobal.com

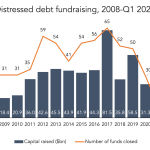

Timing is key in distressed debt The global pandemic provided another reminder that moving fast when opportunity arises is vital for managers in the space. When covid began spreading swiftly around the world early last year, a key facet of distressed debt investing was reinforced – the importance of timing. As public and private markets…

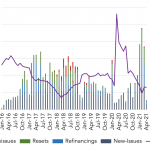

US$93.8bn of CLO issuance priced and closed in 2021 to date In another indication of robust leveraged loan market activity in 2Q, the CLO calendar continues to grow at a record pace. There has been US$148.4bn of US CLO volume recorded so far in 2021, split between US$54.6bn of new issues, US$53.3bn of refinancings and…

Private debt is a relatively recent entrant to the alternative asset class. In 2007 private debt AUM measured less than $200 billion. Today illiquid credit is $900 billion with growth estimates of 50% over the next 5 years. The Lincoln Senior Debt Index provides lenders and investors a much-needed tool to assess portfolio performance and […]

Source: LevFin Insights Source: LevFin Insights Source: Lipper (Past performance is no guarantee of future results.) Contact: Robert Polenberg robert.polenberg@levfininsights.com

Percentage of Loans with F&C Tranche Growers (Past performance is no guarantee of future results.) Contact: Steven Miller

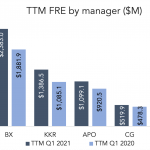

A good start to the year for public PEGs Download PitchBook’s Report here. The “Big Five” PE firms that trade publicly—Blackstone, KKR, Apollo, Carlyle and Ares—had an impressive start to 2021. PitchBook’s latest analyst note takes a close look at their Q1 2021 financials, which showed sustained momentum coming out of the pandemic late last year….

Remote due diligence is here to stay The challenges of life away from people and offices may have hindered private debt fundraising to an extent, but video meetings also have their supporters. Fundraising these days is a tough slog, right? Well certainly for private debt anyway, even if the still-surging private equity asset class managed…

“Thank you for this series. I’m curious how the benchmark accounts for where the loan is in the cap structure? For example, recovery rates for unitranche, 1st lien and second lien are different. Any portfolio would have to match the composition to effectively compare against the benchmark. Otherwise, you would need different benchmarks for each.”…