Beyond structural pressures, liquidity mismatches, and conflation with large cap strategies, the most fundamental question for any credit investor: What is the actual risk of losing money?

Structural protections are built into core middle market (CMM) loans because they are illiquid and intended to be held to maturity. Unlike large cap cov-lite deals, CMM loans have financial covenants testing borrowers’ ongoing performance, meaning that lenders get early warning and intervention rights before the asset reaches the point of impairment...

Quote of the Week

“While there are signs of pressure in certain [private credit] segments, overall levels remain relatively contained and continue to track below those in the broadly syndicated loan market.” – Stephen A. Boyko, Proskauer (Bloomberg News).

Featuring Charts

Chart of the Week: At Any Rate

Default metrics aren’t created equal. How a default is defined and measured can tell very different stories — so knowing what’s behind the number matters as much as the number itself. Source: BofA Global Research.

Read More

Chart of the Week: Queue Here

Investor education is becoming critical as quarterly redemption limits are being tested. Source: Data is derived from publicly available information, including U.S. Securities and Exchange Commission filings.

Read More

Chart of the Week: Ex Uno, Plures

Unlike the US, private credit began as one entity and morphed into many states. Source: Apollo Outlook For Public and Private Markets (April 2026)

Read More

Chart of the Week: Different Strokes

Core and LMM portfolio overlap has remained relatively stable over the past decade. Source: Company filings and Raymond James research

Read More

Chart of the Week: Leverage Takeover

Middle market buyout financings increasingly dominated by direct lenders. Source: LSEG LPC. Middle Market LBO volume.

Read More

Chart of the Week: Perception is Reality

Investors bombarded with scary headlines worrying less about real private credit risks. Source: PitchBook

Read More

Subscribe Now!

Join the leading voice of the middle market. Try us free for 30 days.

Click here to view the Newsletter sample.

What is the Lead Left?

- One-stop source for deals and data

- Market trend commentary and analysis

- Exclusive interviews with thought leaders

View Article By

Features

Bloomberg: Leveraged Lending Insights – 4/27/2026

US Leveraged Loan Issuance Continues Decline in April New issuance continued to trickle in this April, with just $25.06b priced through the 29th, down approximately 15% form last month’s figure of $29.6b and amounting to the lowest level of issuance since April 2025 when just $7.9b priced following “Liberation Day” tariffs…. Subscribe to Read MoreAlready

Octus: Private Credit & Deal Origination Insights – 4/27/2026

Consumer Discretionary Overtakes Information Technology as Top Nonaccruals Sector by Number of Issuers in Q4’25 To request access to the full analysis, please visit here…. Subscribe to Read MoreAlready a member? Log in here...

Middle Market & Private Credit – 4/27/2026

US BDCs Face Persistent Earnings Pressure and Asset Quality Risks Click here to learn more. U.S. business development companies (BDCs) face increasing pressure in 2026 as slower capital inflows and elevated redemptions weaken liquidity, while competitive underwriting and interest rates weigh on asset quality and earnings…. Subscribe to Read MoreAlready a member? Log in here...

The Pulse of Private Equity – 4/27/2026

US PE EV/EBITDA multiples Download PitchBook’s Report here. Global buyout valuations have held steady through the opening months of 2026, with TTM EV/EBITDA multiples hovering near the levels seen during 2024’s recovery and 2025’s subsequent plateau…. Subscribe to Read MoreAlready a member? Log in here...

Leveraged Loan Insight & Analysis – 4/27/2026

Refinancings drove record 1Q26 US ABL volume, excluding the 1Q23 LIBOR/SOFR surge US syndicated ABL activity rose sharply in 1Q26, with total issuance reaching US$29.9bn, up 31% year-over-year and marking the strongest first quarter on record when excluding the LIBOR‑to‑SOFR transition driven surge in 1Q23…. Subscribe to Read MoreAlready a member? Log in here...

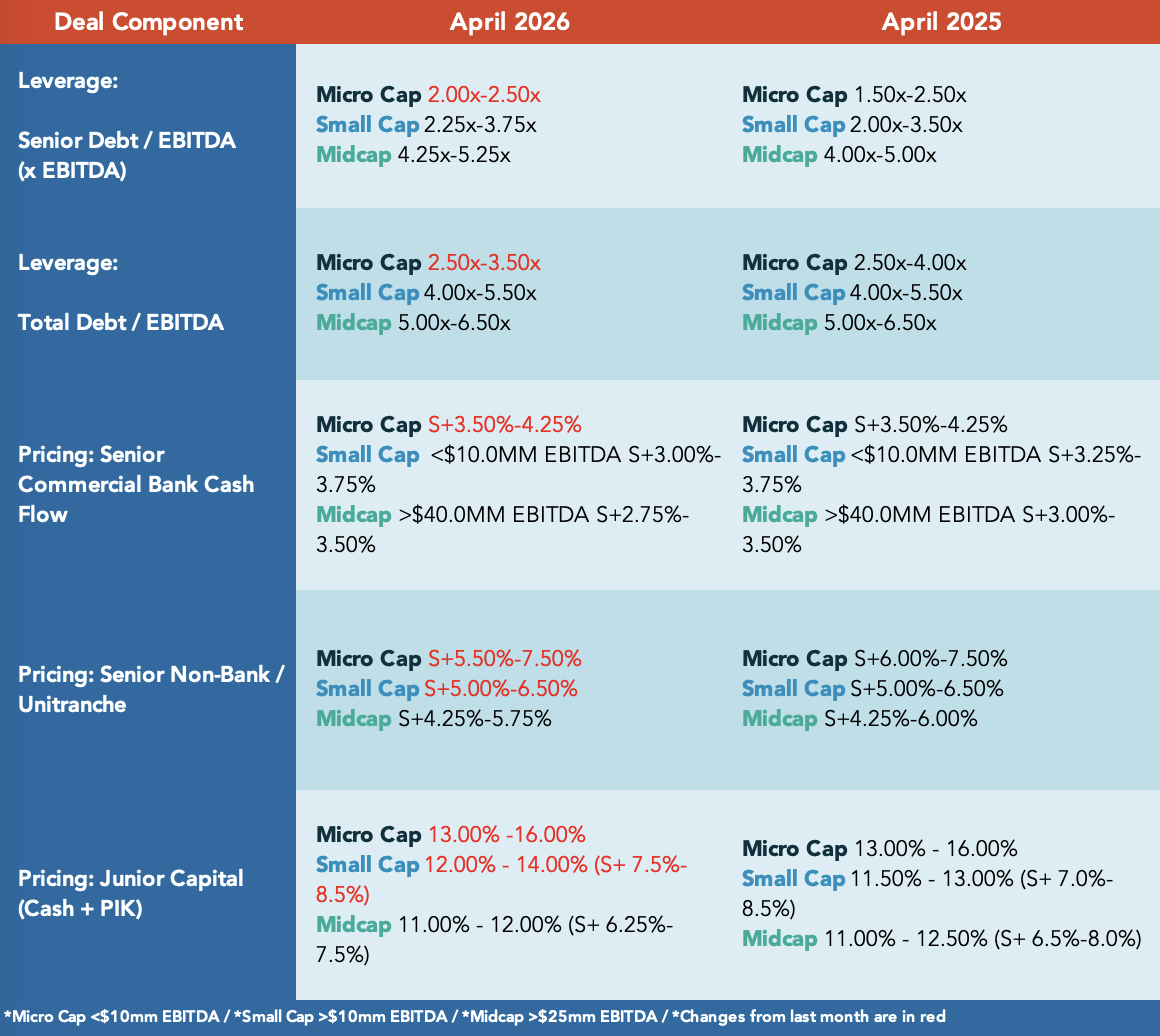

Middle Market Deal Terms at a Glance

provided by

![]()

Beginning in July 2022 The Lead Left published a series of articles on credit market. This report consolidates those articles.

Cov-lite trends Inflation & rising interest rates – LIBOR to SOFR transition Mega-tranche uni trend ESG takes center stage Login to view interactive report and download PDF version. … Subscribe to Read MoreAlready a member? Log in here Related posts: 2H 2021 Midyear Outlook Report State of the Capital Markets – Fourth Quarter 2016 Review and

Beginning in September 2021 The Lead Left published a series of articles on supply chain. This report consolidates those articles.

Our Content Partners