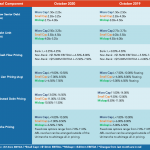

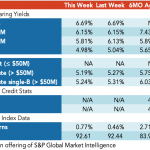

Middle Market Deal Terms at a Glance – October 2020

Source: SPP Capital Partners Contact: Stefan Shaffer stefan@sppcapital.com

Source: SPP Capital Partners Contact: Stefan Shaffer stefan@sppcapital.com

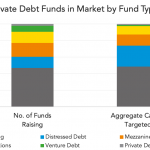

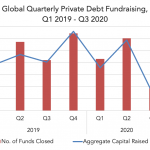

Record Amounts of Funds and Capital in the Private Debt Market The number of private debt funds in market and the capital targeted have reached new records at the beginning of Q4 – 521 funds in market seeking for a combined $295bn. This is a 54% increase compared to January 2020, when funds on the…

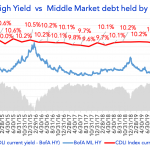

Source: Cliffwater Direct Lending Index and BofA Merrill Lynch US High Yield Effective Yield The red line in the chart is the *Cliffwater Direct Lending Index (CDLI) current yield, which is based on the investment income of the underlying assets held by public and private BDCs. BDCs invest in middle market companies, and the Index…

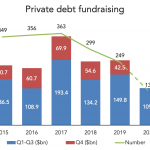

Fundraising has not been stopped in its tracks Senior debt strategies lead the way as capital accumulation manages to retain some forward momentum. Private debt funds raised a total of $109.8 billion during the first nine months of 2020, the lowest figure since 2016, according to PDI data (see chart above)…. Subscribe to Read MoreAlready

Contact: Marina Lukatskymarina.lukatsky@spglobal.com

3Q20 MM sponsored loan issuance picks up from 2Q20’s low, but still quite anemic Sponsor-backed middle market volume showed a pick up in 3Q20 to US$5.6bn, up 120% from 2Q20’s post credit crisis low. But volume was still quite dire and over 62% behind 3Q19’s level. While pricing has been tightening dramatically month after month,…

A recent note from our good friend at Bloomberg, Kelsey Butler, pointed to a study in Astrobiology highlighting 24 planets that could sustain life. Criteria for “superhabitability” include home stars younger than the Sun, Earth-like masses, and atmospheres with warmth and moisture greater than Earth. All these planets are over 100 light years away –…

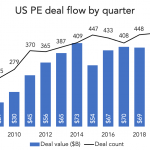

Carveouts – up but not booming Download PitchBook’s Report here. One of the earliest predictions back in March was that PE-led carveout activity would go up. PEGs had dry powder to spend and corporate sellers had liquidity concerns—they were also going to need to concentrate on their core businesses, so it made intuitive sense than ancillary…

The number of private debt funds raised globally slumped in the third quarter, but has generally held steady.