The Case for Covenants (Part Four)

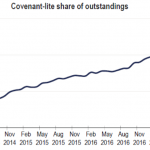

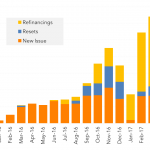

It’s not surprising so much fuss has been made about the proliferation of cov-lite structures in the leveraged loan market. After all, what was the exception even among larger issuers has become the rule (see our Chart of the Week). Indeed this trend has been growing since 2013 when almost 60% of loan volume lacked…