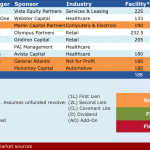

Select Deals in the Market – 7/10/2017

☞ Click for a larger image.

☞ Click for a larger image.

Middle market loan volume disappoints in 2Q17 Despite all the capital flowing into the middle market, loan supply continued to disappoint in 2Q17. Total middle market loan issuance reached US$39.8bn in 2Q17, up a slight 2% and 7% from 1Q17 and 2Q16 levels…. Subscribe to Read MoreAlready a member? Log in here...

Contact: Steven Miller smiller@covenantreview

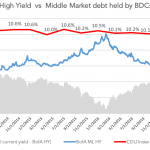

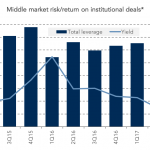

Source: Cliffwater Direct Lending Index and BofA Merrill Lynch US High Yield Effective Yield The red line in the chart is the *Cliffwater Direct Lending Index (CDLI) current yield, which is based on the investment income of the underlying assets held by public and private BDCs. BDCs invest in middle market companies, and the Index comprises of more…

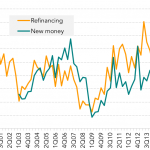

If sheer volume means anything, total syndicated loan activity in the US for the first half of the year was singular. According to Thomson Reuters LPC, more than $1.2 trillion of paper – both investment and non-investment grade – was distributed through June 30. That was a bigger number than any other half-year on record. Digging…

Mega-funds on the Comeback For a preliminary peek at second quarter PE numbers in PitchBook’s upcoming Breakdown Report, please refer to the linked infographic. Through the first half of the year, mega-funds of $10 billion or more in size have made a strong comeback in the U.S. and Europe. Five such private equity funds have already…

This week we chat with George Majoros, Jr., Co-Managing Partner, EagleTree Capital (formerly Wasserstein Partners). Mr. Majoros joined the original predecessor firm Wasserstein Perella in 1993. He currently serves as Chairman of the Boards of Directors for Paris Presents and Jamberry Nails and is a member of EagleTree’s Investment Committee. Since 2001, the team has…

Contact: Timothy Stubbs timothy.stubbs@spglobal.com

Review of Current Market Conditions/ Analysis of Capital Markets Metrics/ Review of Credit Quality/ Outlook for Third Quarter 2017

Since early last year, leverage vs. yield for middle market institutional loans has deteriorated in favor of the issuer.