Special Report: Why Sponsors Matter

Beginning in September 2016 The Lead Left published a series of articles on sponsors. This report consolidates those articles.

Beginning in September 2016 The Lead Left published a series of articles on sponsors. This report consolidates those articles.

The notion that the middle market has reached a level of maturity was supported by a plethora of evidence this past year. For one thing, arrangers showed astonishing underwriting capacity by taking on a number of large-cap sponsored buyouts. Probably the most precedent-setting was Qlik Technologies. At just over $1 billion, this Ares-led unitranche represented a…

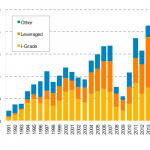

Just shy of US$2tr 2016 US syndicated loan volume is flat year over year

US arrangers pushed almost US$2 Tr through retail syndication in 2016, levels on par with 2015 totals but down modestly compared to the US$2.1tr raised in 2014. The year got off to a slow start as the market volatility that was observed in the oil and gas and commodities sectors in late 2015 carried over to the first quarter of 2016, dampening lender appetite and limiting the pipeline of deals...

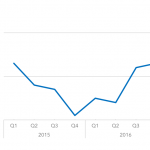

Average Free-and-Clear Tranche as a Multiple of PF EBITDA

☞ Click for a larger image.

This week we continue our conversation with Andrew Brady, Managing Director and Leveraged Loan Portfolio Manager of Marathon Asset Management, L.P. Marathon is a global credit manager with approximately $13 billion of capital under management investing in the global credit markets. Second of two parts – View part one The Lead Left: You mentioned health care. What…

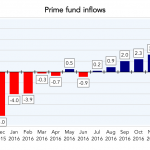

The second half of 2016, climaxing in December’s Fed hike, saw leveraged loans find increasing favor with institutional investors.

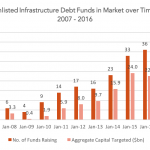

Infrastructure Debt Rises in Prominence

Although banks are the primary providers of financing for global infrastructure projects, liquidity and capital requirements can prevent them from fully serving the market. This has led to an opportunity for the unlisted fund management industry to become a significant niche player in the provision of debt financing for infrastructure...

What is in store for US private equity in 2017?

After a high-water mark for US private equity activity in 2015, last year experienced a significant slowing in not only the number of closed deals but also total deal value, the latter ameliorated by a bevy of blockbuster transactions. This was driven in part by the progression of a typical investment cycle, wherein after a steady ramp-up in dealmaking the market attracts more and more firms looking to cut deals and consequently becomes pricier...