Middle Market Deal Terms at a Glance – Oct 2016

Source: SPP Capital Partners Contact: Stefan Shaffer stefan@sppcapital.com

Source: SPP Capital Partners Contact: Stefan Shaffer stefan@sppcapital.com

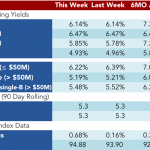

Influx of second-lien issuance has investors pushing back on terms

Recently, investors have been more open to the lower rated, higher return type of loans that were more scarce earlier in the year. In particular, second-lien issuance has picked up. Just two weeks into October and there has already been US$1.5bn in completed second-lien loan issuance which would account for 57% of second-lien issuance for all of 2Q16. This influx of higher yielding assets into the market has caused more push back from investors during negotiations...

Driven by a benign credit environment and favorable relative value dynamics, $2.5 billion has flowed into retail loan funds.

News reached us over the weekend of a new trend in baseball. Apparently several Chicago Cubs relievers are applying copious amounts of perfume as a good luck charm. Turns out players from last year’s Kansas City Royals did the same thing. And they won the World Series. The Cubs manager tweeted, “Aroma still matters.” A…

☞ Click for a larger image.

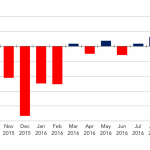

Average First Lien Headroom under Debt Incurrence Test Based on Initial PF Leverage, YTD Contact: Steven Miller smiller@covenantreview.com

Contact: Timothy Stubbs timothy.stubbs@spglobal.com

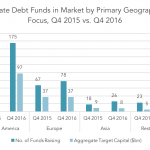

Private Debt: Funds in Market

Preqin’s quarterly update on the private debt industry finds that as of the beginning of Q4 2016, there are 304 funds in market targeting an aggregate $147bn globally. With few funds closing through the year to date, the marketplace has grown considerably since mid-year; there are 50 more vehicles on the road seeking an extra $6bn of investor commitments compared to the start of Q3.

Direct lending, once again, represents the largest proportion of private debt funds on the road, both by number (38%) and aggregate capital targeted (39%)...

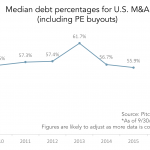

Debt Usage in US M&A Remains Historically Low

Even as multiples remain stubbornly high across multiple sectors, debt usage remains low. This is primarily the result of a confluence of factors, including stricter regulations, cash-rich buyers and a general trend toward buying and building as a strategy on the part of private equity investors. In that last case, PE firms aren’t relying as much on financial engineering as they used to, looking instead to deploying more equity in deals to avoid overburdening portfolio companies with barely serviceable debt loads. Of course, that necessitates shrewd operational enhancements...