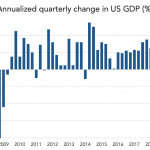

Chart of the Week: End of a Cycle

The onset of COVID-19 also signaled the expansion’s end; 1Q GDP slumped 4.8%, worst since 2008.

The onset of COVID-19 also signaled the expansion’s end; 1Q GDP slumped 4.8%, worst since 2008.

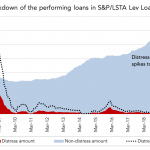

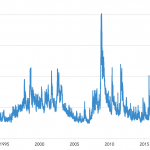

When secondary leveraged loan prices cratered last month, the resulting distressed volume outweighed all 2008-09 loans.

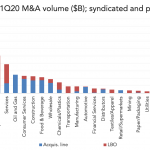

Defensive industries such as business services, healthcare, tech, and A&D led all sectors in 1Q M&A volume

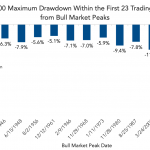

Last month’s early price plunge was three times worse than the Great Depression.

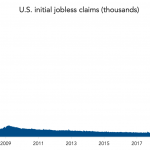

US jobless claims totaled 10 million in two weeks; it took six months to hit those levels during the Great Recession.

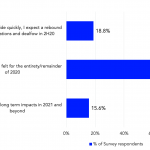

A recent Refinitiv lender survey revealed expectations of a quick COVID-19 resolution is unlikely.

No question future growth will be off big-time; just how bad, and for how long, is unknown.

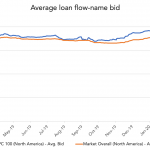

The average bid for the most liquid leverage loans cratered as the effects of the coronavirus have taken hold.

The VIX index of volatility hit a post-recession high in the 40’s this week amid coronavirus concerns.

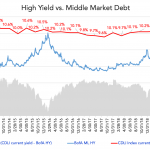

Senior direct loans in BDCs have maintained a steady 10% yield, better than high-yield bonds.