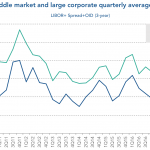

Chart of the Week: Mid Cap Gap

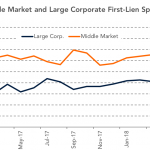

All-in spreads favored middle market loans over large caps by 117 bps in September (up from 97 bps in August), while Libor remained flat.

All-in spreads favored middle market loans over large caps by 117 bps in September (up from 97 bps in August), while Libor remained flat.

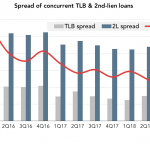

An examination of all-market spreads show that unitranches to be higher than first/second lien, but the differential is shrinking.

New issue first and second lien spreads are on the rise, though the differential is shrinking.

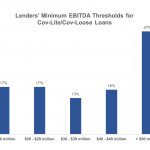

In a William Blair survey, 63% of lenders indicated they would consider cov-lite or cov-loose structures for issuers below $50 million in ebitda.

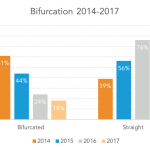

According to Proskauer Rose, the vast majority of its private credit clients are employing non-bifurcated unitranche structures.

The illiquidity premium earned by middle market loans over broadly syndicated ones has generally tightened, now at less than 70 bps, while all-in spreads have risen.

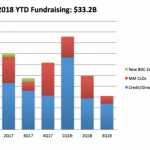

After a hot first quarter, fundraising for middle market vehicles has slumped a bit, though still on track for a strong year.

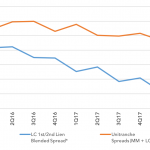

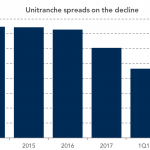

As all-in senior debt spreads have compressed, so have blended spreads for one-stop credit solutions.

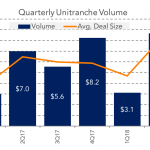

Single-tranche senior debt financing volume and deal size rose sharply last quarter as direct lenders found traction with one-stop solutions.

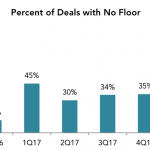

With Libor higher than the historic 1% leveraged loan floor, the rationale for that rate subsidy is going away.