Chart of the Week: Capital Source

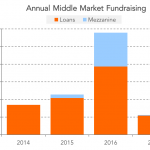

So far this year fundraising for middle market firms is matching the pace we saw in 2016.

So far this year fundraising for middle market firms is matching the pace we saw in 2016.

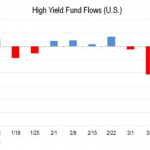

Dropping oil prices and last week’s Fed rate hike caused investors to push almost $5.7 billion out of high-yield accounts; totaling $8 billion in only three weeks.

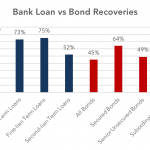

The lower on the capital stack an debt investor’s position goes, the more challenged is the recovery.

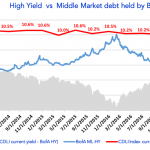

Last year’s downturn-related worries caused bond price and yield swings, while private credit remained relatively insulated from market moves.

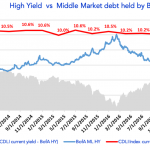

The attractiveness of the middle-market loan asset class is highlighted by its consistent premium over traditional high yield bonds.

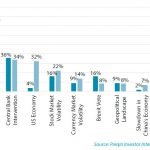

According to Preqin, low interest rates is top factor affecting credit portfolios, with central banks and the US economy next.

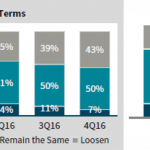

The vast majority of respondents to William Blair’s survey on leverage lending conditions believe leverage and terms will either loosen or remain unchanged.

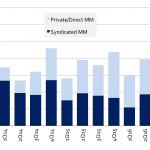

The volume for “new money” loans jumped last quarter (and last year) for both syndicated and privately clubbed middle market transactions.

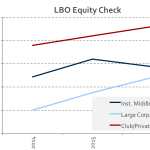

Sponsors for club buyout financings are putting in more equity capital than either their broadly syndicated or larger middle market counterparts.

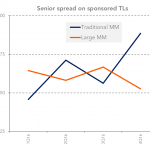

Spreads for facility sizes of $100 million or less approached 500 bps over Libor at year-end; larger deals contracted to around 450 bps.