Chart of the Week: Fall Rising

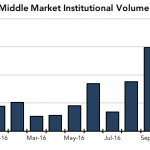

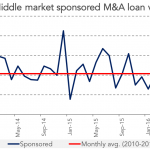

So far in October, middle market loan activity is tracking for its fourth consecutive month-over-month improvement.

So far in October, middle market loan activity is tracking for its fourth consecutive month-over-month improvement.

Driven by a benign credit environment and favorable relative value dynamics, $2.5 billion has flowed into retail loan funds.

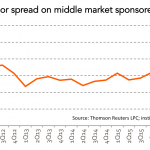

Spreads for middle market sponsored loans have generally remained range-bound around L+500 for the past four years.

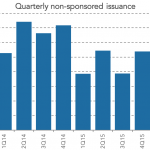

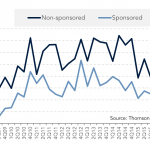

Second quarter non-sponsored loan volume was down 5% from the first quarter but off sharply from the second quarter last year. Source: Thomson Reuters LPC

Monthly loan activity related to middle market buyouts has risen above the five year average for the first time in a year. Source: Thomson Reuters LPC

Loan volume for both sponsored and non-sponsored middle market transactions have generally slumped since 2014. Source: Thomson Reuters LPC

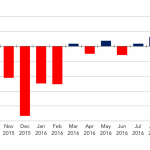

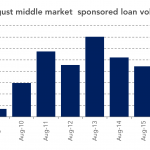

While last month’s loan volume seemed exceptionally slow, it was actually better than 2015’s level, and consistent with the past five years. Source: Thomson Reuters LPC

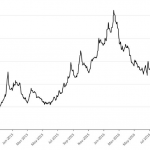

Junk bond spreads have eased this year in the face of continued Fed liquidity and a benign default outlook. Source: Bloomberg LP, The Daily Shot; high yield option adjusted spreads (all sectors)

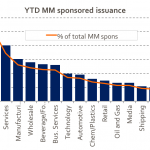

More new middle market sponsored deals have been in healthcare this year than any other sector. Source: Thomson Reuters LPC

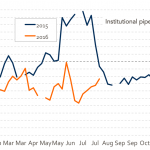

The pipeline for large corporate institutional deals may finally catch up to last year’s levels, after being behind almost all year. Source: Thomson Reuters LPC