Leveraged Loan Insight & Analysis – 3/13/2017

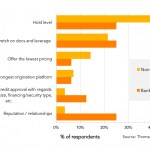

What is the #1 factor to winning a deal in today’s environment?

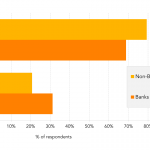

When asked to select the #1 biggest driver in helping them win deals in this increasingly competitive environment, middle market banks were mixed. According to Thomson Reuters LPC's recent survey, one quarter said it comes down to the relationship, especially in the non-sponsored market where issuers rely heavily on that long term relationship. Perhaps more surprising, only 4% of non-banks ranked reputation and relationship as the number one factor. One quarter of banks chose willingness to stretch especially with regard to sponsors who are often asking for large corporate term sheets on smaller deals. One fifth of non-regulated lenders agreed...