Which EBITDA adjustments do you employ/see most frequently?

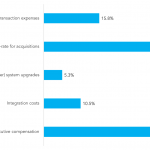

Q: Private Equity Investors: Which EBITDA adjustments do you employ most frequently? Q: Direct Lenders: Which EBITDA adjustments do you see from sponsors most frequently?

Q: Private Equity Investors: Which EBITDA adjustments do you employ most frequently? Q: Direct Lenders: Which EBITDA adjustments do you see from sponsors most frequently?

We tend to be a late adopter of cultural phenomena, so our appreciation of curling was understandably delayed. A sport that plays like shuffleboard, tosses around terms like hack and hog line, and employs practitioners who carry brooms, is a tough sell. But thanks to relentless Olympic coverage, the US men winning a first-time ever…

News reached us last week that the great mathematician, Monty Hall, passed away at the age of 96. Better known as the host of the 1960’s TV hit, “Let’s Make a Deal,” Mr. Hall lent his name to game theory for the so-called 3-Door Monty Hall Problem. Behind three doors there’s a brand new car,…

Our story last week of the hundred-year old fruitcake captured readers’ attention. Tributes to this underappreciated treat poured into the Lead Left mailbox. “It’s believed there’s only one fruitcake in existence,” one friend wrote. “It gets passed around during the holidays from family to family. Now we all know where it came from.” There’s also…

At a recent debt conference we did what most of our direct lending colleagues are doing these days: complain. Speaking with one long-time practitioner, we mentioned a middle market transaction which was both cov-lite and ebitda adjustment-heavy. “Yeah, it’s ridiculous,” he said. “But it’ll get done.” Therein lies the problem. As we discussed last week, loan…

Last week we punctured the myth that the influx of new private debt funds is creating excess demand for the level of deal supply of middle market senior loans [link]. We now turn our attention to credit quality. How will this year fare for credit investors relative to years past, and expectations? First, let’s separate…

“How’s your pipeline?” we asked the head of one of the leading middle market arrangers in December. He shook his head. “The quality-adjusted deal flow is down.” That distinction resonated with a number of our middle market brethren. Complaints centered around ebitda adjustments, over-liberal debt allowance baskets, and covenant-lite (or covenant-wide) structures. “High leverage per…

News reached us over the weekend of a new trend in baseball. Apparently several Chicago Cubs relievers are applying copious amounts of perfume as a good luck charm. Turns out players from last year’s Kansas City Royals did the same thing. And they won the World Series. The Cubs manager tweeted, “Aroma still matters.” A…

Leveraged lending guidelines have set six times total leverage as the limit above which a loan would likely be criticized by examiners. Less noted by the media, but of growing interest to market players, are the components of leverage metrics; specifically, how the numerator (debt) and the denominator (cash flow) are being massaged to put…