The Case for Junior Capital (Last of Four Parts)

In early 2020, just before Covid came crashing down on our heads, we were in the middle of a Lead Left series called “Ten Top Myths About Private Credit”. Myth #5, published on February 20, was “No one uses mezzanine debt anymore.”

We felt compelled, after a decade of increasingly aggressive senior and unitranche financings, to point out how private equity sponsors had never stopped using junior debt as “patient capital” to help stretch leverage and provide a cushion to banks and other senior lenders…

▶︎ Read July 31 2023 newsletter: here

▶︎ Chart of the Week: here (by PE Buyout & Mezzanine – Cambridge Associates, MM direct lending; Cliffwater CDLI, High yield; ICE BofA US High Yield Index, Broadly syndicated; S&P/LSTA LL)

(Any “forward-looking” information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.)

Latest news

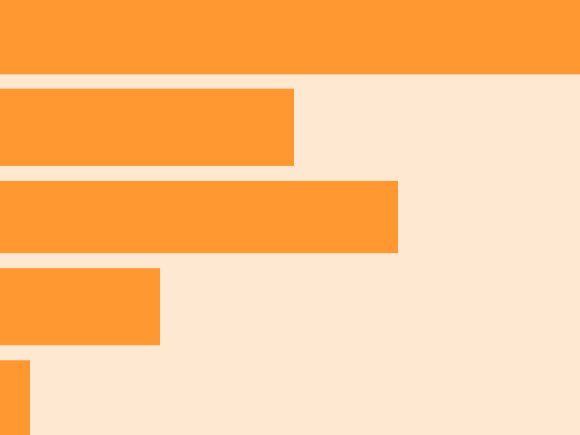

PE middle-market pooled IRR and TVPI by TEV size bucket

The lower end of the middle market has generated better returns on average and does not come with significantly more left-tail risk

Investors exit retail loan funds in July

Investors in leveraged loans have been pulling money from retail funds in recent weeks, with redemptions outpacing investments by $253.3b…