Chart of the Week: Mega Billions

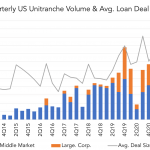

Volume for unitranche financings slumped at Covid’s onset, but quickly recovered.

Volume for unitranche financings slumped at Covid’s onset, but quickly recovered.

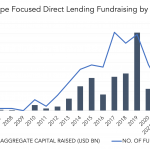

Fundraising for European direct lending almost doubled since 2015, hit Covid, but is on the mend.

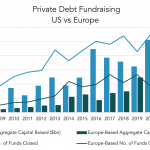

Fundraising for private debt in both US and Europe was strong coming into Covid, fell off, but is recovering.

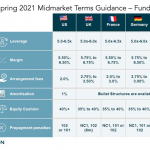

Lincoln’s illustrative terms for “reasonably strong” senior and unitranche credits are generally consistent by country.

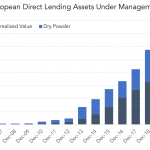

Non-bank European lending AUM is almost $160 billion, including about $50 billion of dry powder.

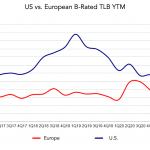

The relative yields-to-maturity of institutional term loans in the US vs. Europe have narrowed during Covid.

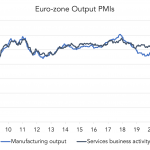

As in the US, European manufacturing and services has jumped higher than pre-Covid levels.

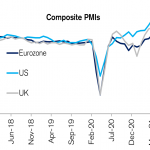

The European economy is coming back in sync with the US; the UK is the growth engine.

Despite the threat of higher prices, long-term interest rates have eased, supporting bonds of all stripes.

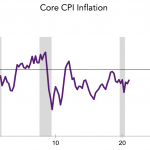

Inflation has been quiescent for over a decade, thanks to a weak economy leading into Covid.