Chart of the Week: Default Lines

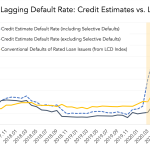

Credit estimates, compared to credit ratings, have proven more beneficial to middle market CLO defaults.

Credit estimates, compared to credit ratings, have proven more beneficial to middle market CLO defaults.

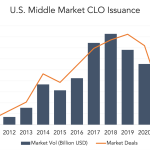

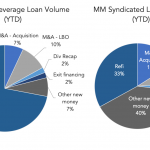

While 2020 middle market CLO activity slid from the previous year, 1Q 2021 issuance has revived.

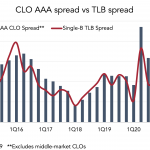

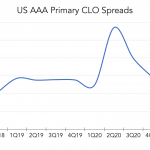

CLO asset and liability spreads move in concert, down now below pre-Covid levels.

CLO liability spreads for the most creditworthy tranches have fallen below pre-Covid levels.

Formation of new collateralized loan obligations slowed last year, but picked up in 2021.

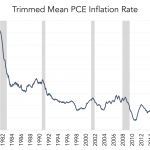

The difference between the five-year Treasury and five-year TIPS shows inflation expectations higher than the Fed’s 2% target.

Since the Volcker Shock of 1980 consumer prices have fallen to a range of 2-3%.

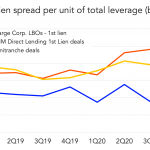

Recently compressed loan spreads leading to more BSL repricings; middle market is lagging.

Expectations for an improved economy has driven yields and time to a Fed hike in opposite directions.

First-lien middle market direct lending deals proved the best value vs. large cap and unitranches.