Chart of the Week: Stretch Marks

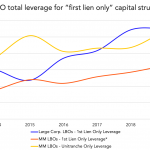

Leverage for middle market unitranches has matched first-lien large cap leverage.

Leverage for middle market unitranches has matched first-lien large cap leverage.

The volume of middle market spread flex-ups at $2.2 billion was the highest in four years.

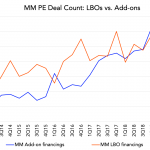

The number of add-ons is more than buyouts, as private equity strives to improve investment returns.

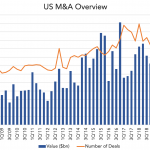

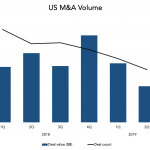

Valuations have trended up over the past decade, but the number of M&A transactions has slowed.

After a strong fourth quarter last year, quarterly US M&A volume has slowed.

Despite lower rates and higher spreads, CLO formation is on track for a good year.

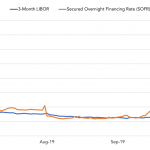

SOFR has hovered around LIBOR, but spiked when repo rates jumped last month.

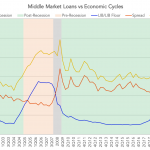

The historic relationship between Libor and midcap loan spreads has been inconsistent.

Since July’s Fed’s rate cut, non-disappointing economic data has boosted Treasury yields.

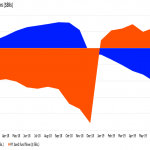

As the Fed reversed course on interest rates last year, cash fled loan funds and piled into high-yield bond accounts.