Markit Recap – 4/25/2019

Argentina and Turkey are firmly established as miscreants in emerging market credit. Both sovereigns have pollical and economic frailties that place them in the highly vulnerable bracket…. Login to Read More...

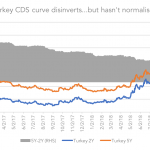

Argentina and Turkey are firmly established as miscreants in emerging market credit. Both sovereigns have pollical and economic frailties that place them in the highly vulnerable bracket…. Login to Read More...

Economics undergraduates know that credibility is vital for monetary policy. But this fact is seemingly elusive for Turkey and their President Tayyip Erdogan. The sovereign is in the midst of yet another crisis,… Login to Read More...

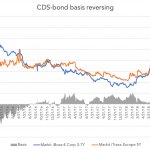

Seasoned credit investors are painfully familiar with shareholder-friendly actions. Leveraged buyouts, debt-financed share buybacks and special dividends can all deliver nasty surprises to bondholders. But idiosyncratic risk works both ways and companies can implement policies that favour bond investors,much to the chagrin of equity holders. Marks & Spencer is a good example…. Login to Read

2018 ended on a sour note and spreads looked set to continue their ascent throughout this year and beyond. But here we are, a little over a week into 2019, and the Markit iTraxx Europe is 10bps tighter than Dec 31 levels. A bumper non-farm payrolls report, a more dovish stance from the Federal Reserve,…

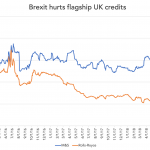

When market makers start sending runs based on nation states rather than sectors it may be a harbinger of fundamental change in how European credit is traded. That is precisely what we are seeing as the Brexit process descended into chaos. A number of UK cabinet members have resigned in protest at Theresa May’s draft…

Mario Draghi, in a press conference confirming that market rate expectations were intact, stated that the risks to the eurozone’s economy are “broadly balanced”. His view may have merit, but there is little doubt that the situation is looking more precarious than a few weeks ago. If negative sentiment does permeate the market and spark…

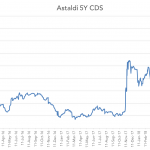

Credit market veterans are all too aware that the determination of CDS credit events is far from straightforward. This can be seen as a weakness of the product, but it is difficult to avoid given the irregularity of bond contracts and the smorgasbord of insolvency laws across different jurisduictions. The case of Astaldi is a…

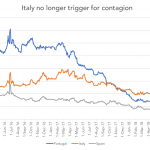

We noted last week that the markets may be guilty of complacency on Italy’s budget, and so it proved. As mooted in the initial spending plan, an increase in the budget deficit to 2.4% was proposed by the government, significantly higher than the 2% limit specified by the European Commission. This was tempered by the…

The appeal of populist, often nativist agenda to electorates disgruntled with economic stagnation and rapid demographic change has been underestimated in recent years, not least by bond markets. Nonetheless, the performance of Italy’s credit spreads over the summer suggests investors are reluctant to wholly embrace political risk aversion…. Login to Read More...

It’s the 10th anniversary of Lehman’s collapse and we are being inundated with retrospectives and predictions of what will cause the next crisis. Many are pointing towards emerging markets as a likely catalyst, a logical conjecture given the tightening in monetary policy that is underway in the US…. Login to Read More...