Chart of the Week: Lost Articles

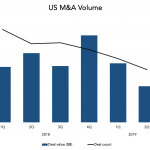

After a strong fourth quarter last year, quarterly US M&A volume has slowed.

After a strong fourth quarter last year, quarterly US M&A volume has slowed.

Despite lower rates and higher spreads, CLO formation is on track for a good year.

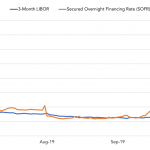

SOFR has hovered around LIBOR, but spiked when repo rates jumped last month.

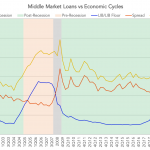

The historic relationship between Libor and midcap loan spreads has been inconsistent.

Since July’s Fed’s rate cut, non-disappointing economic data has boosted Treasury yields.

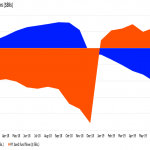

As the Fed reversed course on interest rates last year, cash fled loan funds and piled into high-yield bond accounts.

The average price of a most-liquid broadly syndicated leveraged loan has been within a band most of the summer.

The number of leveraged loans for buyouts over $1 billion has grown steadily since the Great Recession.

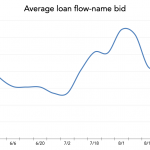

The illiquid non-correlated nature of smaller loans are attractive features amidst today’s market volatility.

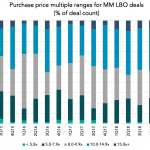

Over half of sponsored transactions are displaying greater than 10x purchase price multiples.