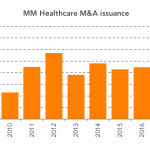

Chart of the Week: On the Mend

Mergers and acquisition financings in the healthcare space for middle market issuers have grown steadily since the credit crisis.

Mergers and acquisition financings in the healthcare space for middle market issuers have grown steadily since the credit crisis.

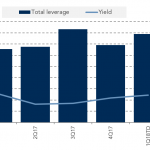

Middle market loans sold to institutional investors are showing higher leverage, but also better yields.

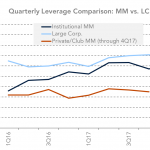

While leverage for institutional middle market LBOs has ticked up over 6x, the club market remains 1.35x lower.

The share of private credit transactions with allowances for incremental debt grows as the issuer ebitda increases.

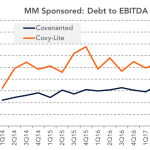

Middle market sponsored loans without maintenance covenants sport leverage a full turn above those with covenants.

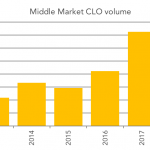

New CLO formation for the coming year is projected by market participants to approach 2017 levels.

Over the past decade, middle market loans showed better loss rates than broadly syndicated ones.

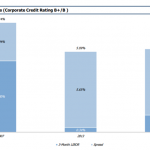

The increase in Libor has caused borrowing spreads to contract, though nowhere near levels seen in 2007.

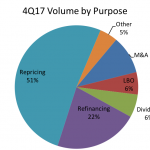

Almost three-quarters of middle market 4Q deals were either repricings or refinancings.

Fundraising last year for middle market lending strategies was dominated by CLOs and credit funds.