Chart of the Week: Buy-and-Building

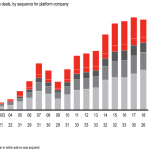

Since the credit crisis private equity sponsors have quickened the pace and number of add-on acquisitions.

Since the credit crisis private equity sponsors have quickened the pace and number of add-on acquisitions.

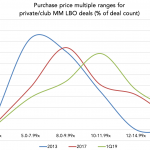

The number of buyouts with purchase price multiples over 10x has increased markedly since 2013.

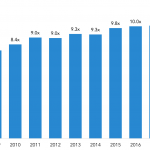

Purchase price multiples eased last year, though still sustained at near record levels.

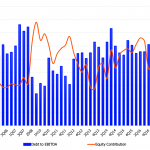

The cost of buying companies has risen for private equity sponsors as a multiple of ebitda since the credit crisis.

After peaking in 2017 at close to 50%, equity share of capital in the middle market has declined to less than 35%.

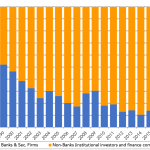

Mergers, consolidations, and regulation all share responsibility for the flight of leveraged loans to the non-bank sector.

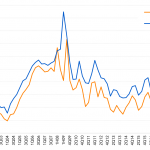

The long-term durability of leveraged loans was demonstrated out of the last recession, as values climbed back to par.

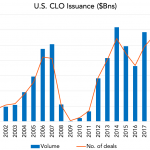

Over time collateralized loan obligations have proven to be resilient through cycles and regulatory hurdles.

After a good run leading up to last year’s market volatility, virtually no names in the LCD LSTA Leveraged Loan Index are trading at or above par.

The premium between large cap and the middle market has shrunk to 50 bps, the tightest in a decade.