Chart of the Week: All-Terrain Vehicles

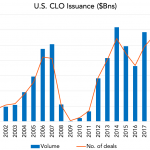

Over time collateralized loan obligations have proven to be resilient through cycles and regulatory hurdles.

Over time collateralized loan obligations have proven to be resilient through cycles and regulatory hurdles.

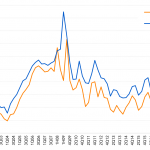

After a good run leading up to last year’s market volatility, virtually no names in the LCD LSTA Leveraged Loan Index are trading at or above par.

The premium between large cap and the middle market has shrunk to 50 bps, the tightest in a decade.

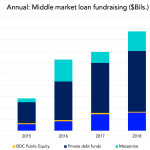

Direct lending has attracted over $275 billion in capital since 2014 across various strategies.

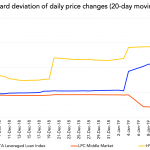

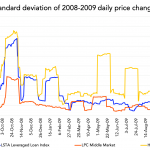

Amid significant price volatility that occupied liquid markets, middle market loan trading levels were relatively stable.

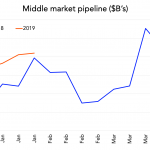

It’s early days, but the middle market pipeline is off to a slightly better start than 2018.

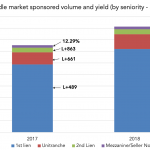

LPC’s analysis of private club deals showed almost 93% of middle market volume was senior or unitranche.

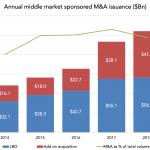

2018 saw another increase in sponsored M&A volume in the middle market; up 12% from 2017.

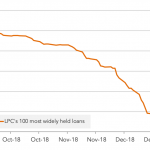

Secondary prices for LPC’s top liquid loans rose almost 2%, as public markets have regained confidence over the past week.

During the worst of the credit crisis the lower volatility of middle market loans is evident, compared to bonds or liquid loans.