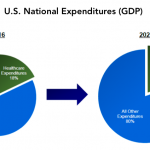

Chart of the Week: Bigger Pie

Two years ago US healthcare expenditures totaled $3.3 trillion; rising to $5.5 trillion by 2025.

Two years ago US healthcare expenditures totaled $3.3 trillion; rising to $5.5 trillion by 2025.

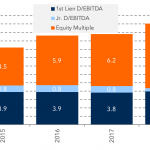

Purchase price multiples for middle market buyouts in the healthcare have risen in the last four years.

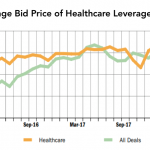

Trading levels of liquid healthcare loans have been down relative to the overall market this year.

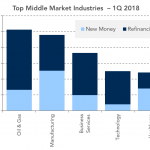

Healthcare rounded out the top five industries for most middle market non-sponsored loan issuance for the first quarter.

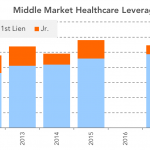

Leverage for mid cap healthcare loans has grown steadily, with senior debt/ebitda now over five times.

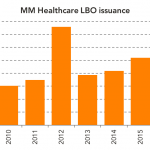

Last year’s volume of financings for middle market healthcare buyouts almost matched 2012’s post-credit crisis record.

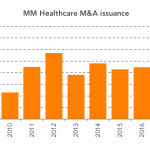

Mergers and acquisition financings in the healthcare space for middle market issuers have grown steadily since the credit crisis.

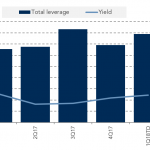

Middle market loans sold to institutional investors are showing higher leverage, but also better yields.

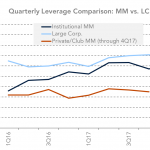

While leverage for institutional middle market LBOs has ticked up over 6x, the club market remains 1.35x lower.

The share of private credit transactions with allowances for incremental debt grows as the issuer ebitda increases.