Chart of the Week: Forward to the Past

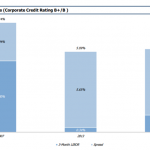

The increase in Libor has caused borrowing spreads to contract, though nowhere near levels seen in 2007.

The increase in Libor has caused borrowing spreads to contract, though nowhere near levels seen in 2007.

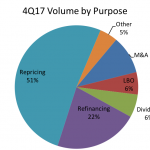

Almost three-quarters of middle market 4Q deals were either repricings or refinancings.

Fundraising last year for middle market lending strategies was dominated by CLOs and credit funds.

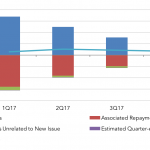

Cash back into investors’ pockets from loan repayments almost offset cash deployed into new loans last year.

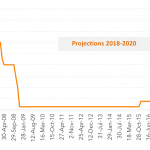

A Fed fund forecast of 2.1% by year end is well below historic levels, not to mention the 5.25% achieved in June 2006.

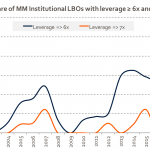

A record 52% of all middle market buyout financings are leveraged at or more than six times ebitda; 15% over 7x.

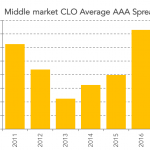

The average spread of the highest-rated middle market CLO liabilities has plummeted over 50 bps since last year.

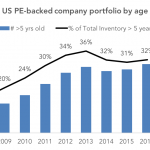

After a three year pause, the number of sponsor-backed portfolio companies held for over five years is rising.

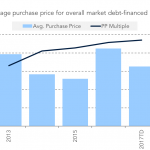

The average buyout price in the overall market has shrunk by $500 million so far this quarter, though it’s up as a multiple of ebitda.

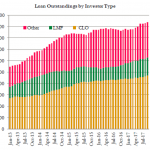

Collateralized loan obligations are still hold the majority of leverage loans, with separate managed accounts on the rise.