Chart of the Week: Growing Gap

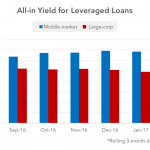

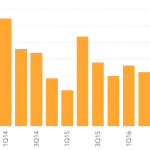

Large liquid loans have been hit with repricings, causing the illiquidity premium for the middle market to approach 200 bps – well above the historic average.

Large liquid loans have been hit with repricings, causing the illiquidity premium for the middle market to approach 200 bps – well above the historic average.

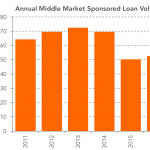

Reported loan activity for sponsor-related syndications rose modestly last year over 2015; private “club” volume expected to be higher.

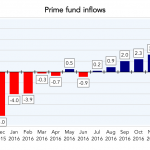

The second half of 2016, climaxing in December’s Fed hike, saw leveraged loans find increasing favor with institutional investors.

Month over month, both October and November have seen improvements over last year in middle market sponsored loan activity.

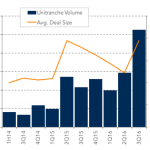

3Q 2016 was the most active quarter in the past several years for unitranche financings, as middle market sponsors increasingly access the non-bank market.

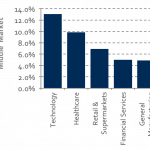

Five sectors comprise 60% of all middle market institutional loans.

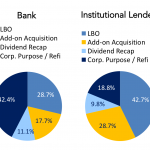

Middle market borrowers look to banks for refinancings; for buyouts and add-ons, almost twice as many seek institutional lenders.

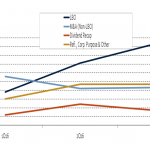

Middle market LBO volume was up 43% for the third quarter, far outpacing the number of add-ons, dividend recaps, and refinancings.

Add-on volume for the overall market rebounded sharply during 2Q 2016 from the first quarter, though slowed last quarter.

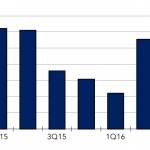

Sponsored acquisition volume for platform companies has averaged less than $2 billion for past five quarters