Chart of the Week – Stall Speed

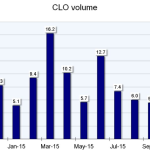

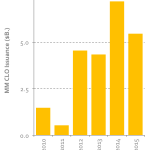

With risk retention rules on the horizon, monthly new CLO issuance has slowed considerably.

With risk retention rules on the horizon, monthly new CLO issuance has slowed considerably.

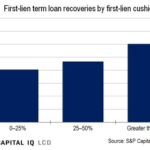

Counterintuitively, recent data from an S&P study show recoveries for first-lien term loans improved only modestly with additional debt capital below them.

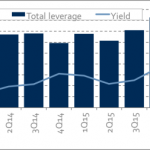

Halfway through the 4Q, middle market deals are showing sharp increases in both leverage and yield. Source: Thomson Reuters LPC; based on cohort of middle market deals with both leverage and yield data.

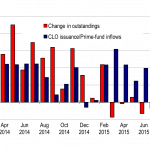

After a strong September, new deal volume eased and demand jumped, creating better technicals in the broadly syndicated market. Source: S&P Capital IQ LCD

Middle market CLO volume $5.5 billion year to date; full year total may fall short of 2014. Source: Thomson Reuters LPC, Wells Fargo

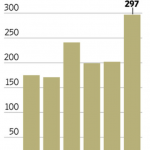

Issuance of private subordinated debt capital has steadily grown since the credit crisis, though last quarter was off the prior number. Source: Thomson Reuters LPC

The number of risk rating downgrades in the corporate sector has hit a five year high – worst since the credit crisis. Source: The Daily Shot, @WSJ Markets

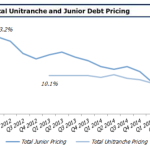

Supply/demand imbalance among unitranche providers continues to keep one-stop pricing below that of junior capital. Source: Lincoln’s proprietary database of over 600 privately-held companies

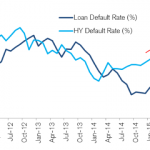

Since early 2014 high-yield default rates have more than doubled, while the same metric for loans remains below 1.5%. Source: Credit Suisse

Cash leaving loan funds has slowed, but still sees nine consecutive weeks of $4 billion outflows.