Leveraged Loan Insight & Analysis -11/14/2016

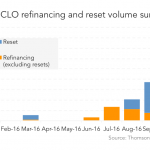

European CLO Issuance

Issuance of European CLOs has reached a post-crisis high as jumbo investments in senior tranches have anchored issuance. European CLOs have seen year-to-date issuance of €14.7 billion across 36 deals, compared with the previous post-crisis high of €14.3 billion in 2014, when 34 deals were completed...