The share of cov-lite middle market leveraged loans is growing relative to larger loans; May’s number is over 60%.

Source: LCD; an offering of S&P Global Market Intelligence

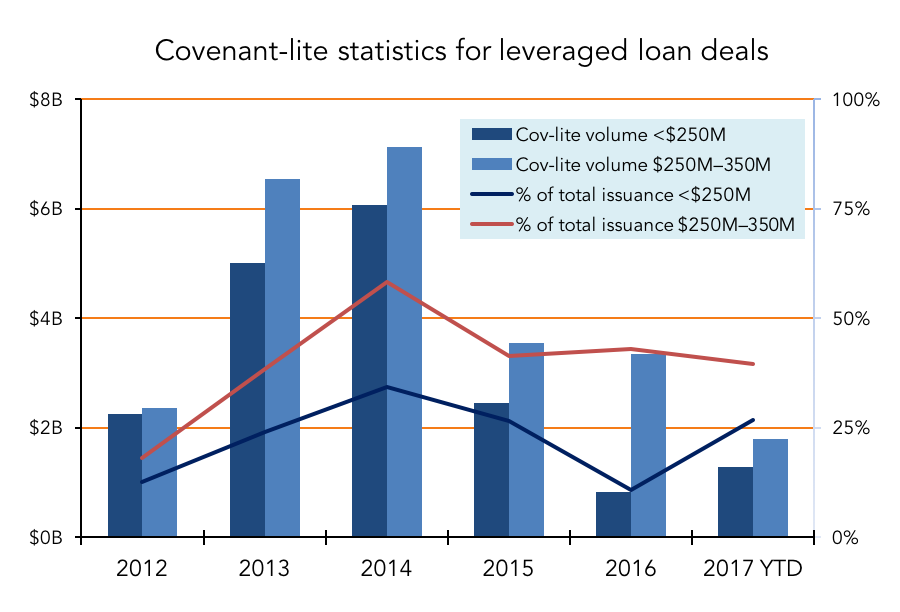

The share of cov-lite middle market leveraged loans is growing relative to larger loans; May’s number is over 60%.

Source: LCD; an offering of S&P Global Market Intelligence

You must be logged in to post a comment.

Permalink

is there a formal definition of “covenant lite”. I understand the concept, but it seems as though it’s a relative concept. To what degree have covenants been weakened since 2008? And is there an expectation of default percentages, impact on pricing and expected recoveries? It seems that underwriters with better, more detailed processes with risk mitigation at the fore will are the ones to partner with. Thoughts?

Permalink

Cov-lite is a misnomer. A more accurate description is “debt incurrence test only.” This is akin to the financial covenants typically part of a high-yield bond issue. Those tests are only triggered when the company incurs additional debt. Leveraged loans carry maintenance test covenants. These are tested every quarter, regardless of new debt.

Covenants have weakened only since about 2013 or so. But that development has accelerated over the past year or so. The room between projected leverage, for example, and actual test levels has widened considerably. Also, the amount of additional debt that can be raised has increased.

Very hard to know the eventual impact on defaults and recoveries. The irony is that cov-lite deals used to be reserved for the best companies, so recoveries were high. The question is will this still be the case with middle market cov-lite.

Totally agree with your last point. It’s all about working with experienced lenders who have been through a cycle and know what you have to do to protect from the downside. And the downside is inevitable; it’s not a question of “if” but “when.”