U.S. Private Credit and Middle Market Performance Monitor: 2Q25

Fitch’s Privately Monitored Ratings Portfolio, Rating Activity

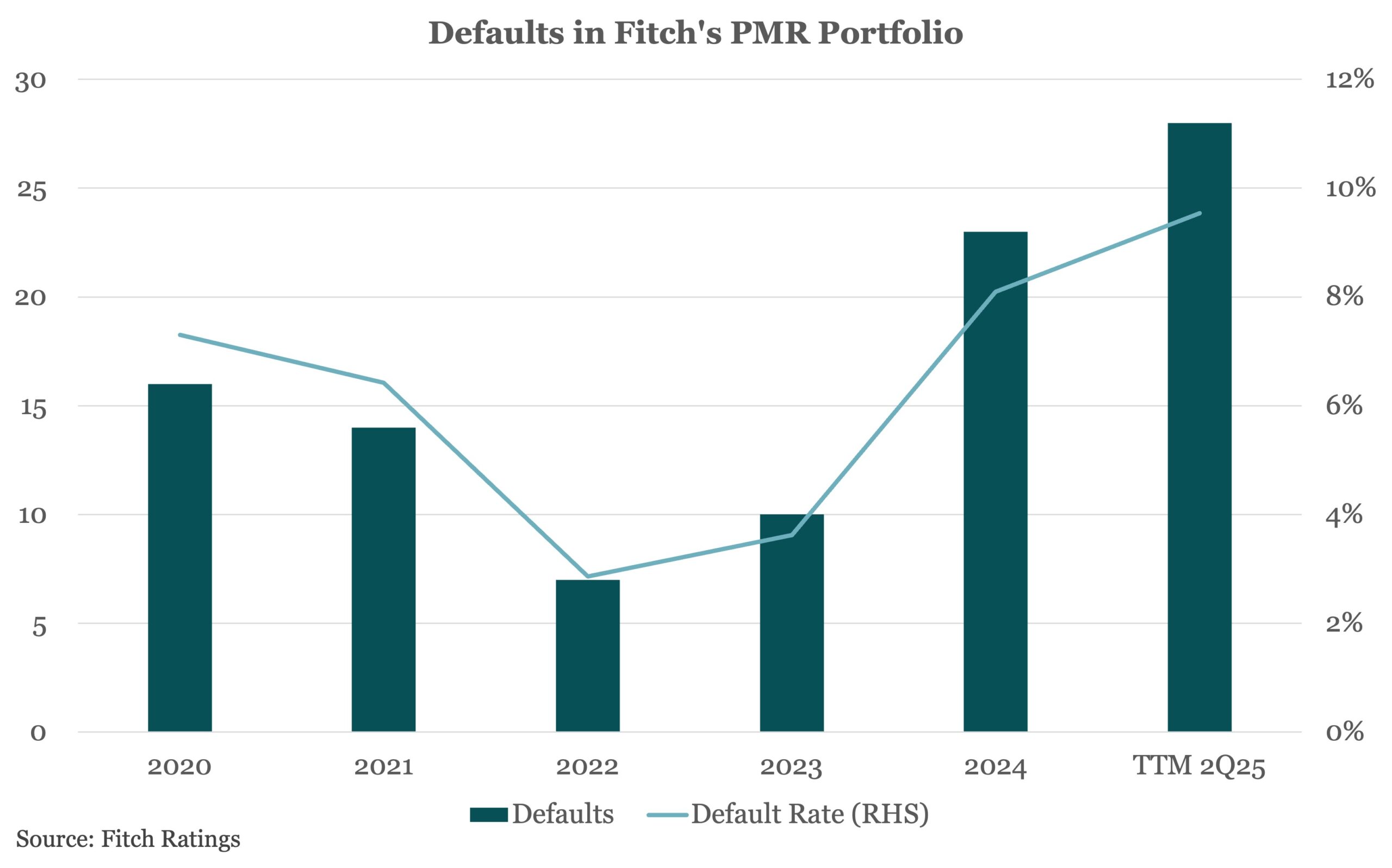

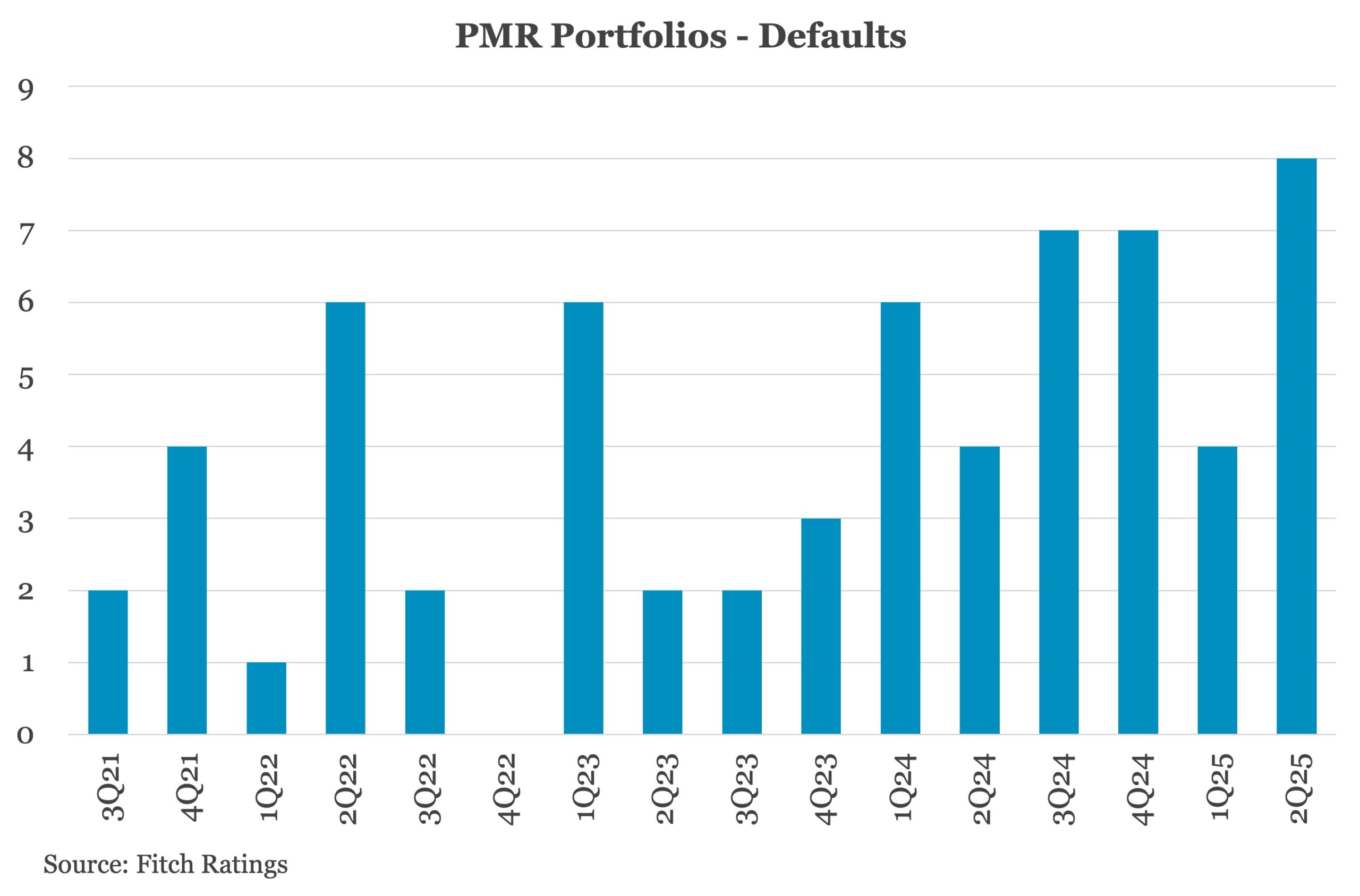

The issuer-weighted TTM default rate for PMRs rose to 9.5% in 2Q25 from 7.8% in 1Q25. Fitch recorded 28 unique defaults for the TTM period, up from 23 in 1Q25. This is the highest default rate since tracking began in 2017. Smaller, private issuers are more vulnerable than larger peers to economic swings, GDP slowdowns, and persistent elevated rates. Their floating-rate structures increase this risk.