Latest Performance Trends for U.S. MM CLOs

Chart

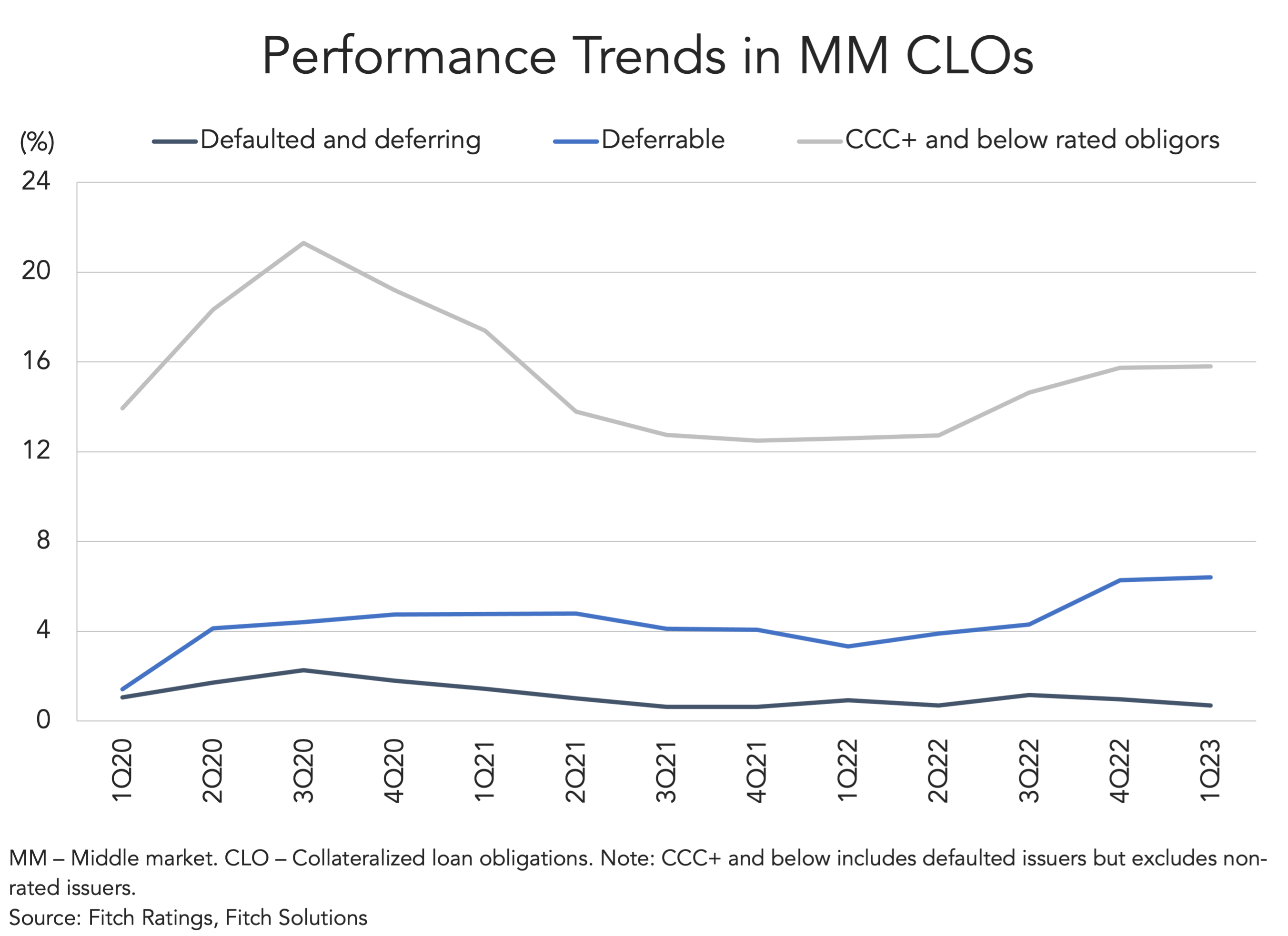

Defaulted and deferring exposure across MM CLOs remained low at 0.7% in 1Q23, while deferrables stood at 6.4%. Exposure to assets rated ‘CCC+’ or below by Fitch Issuer Default Rate Equivalency Rating, as described in Appendix 5 of Fitch’s CLOs and Corporate CDO Rating Criteria, registered at 15.8%.