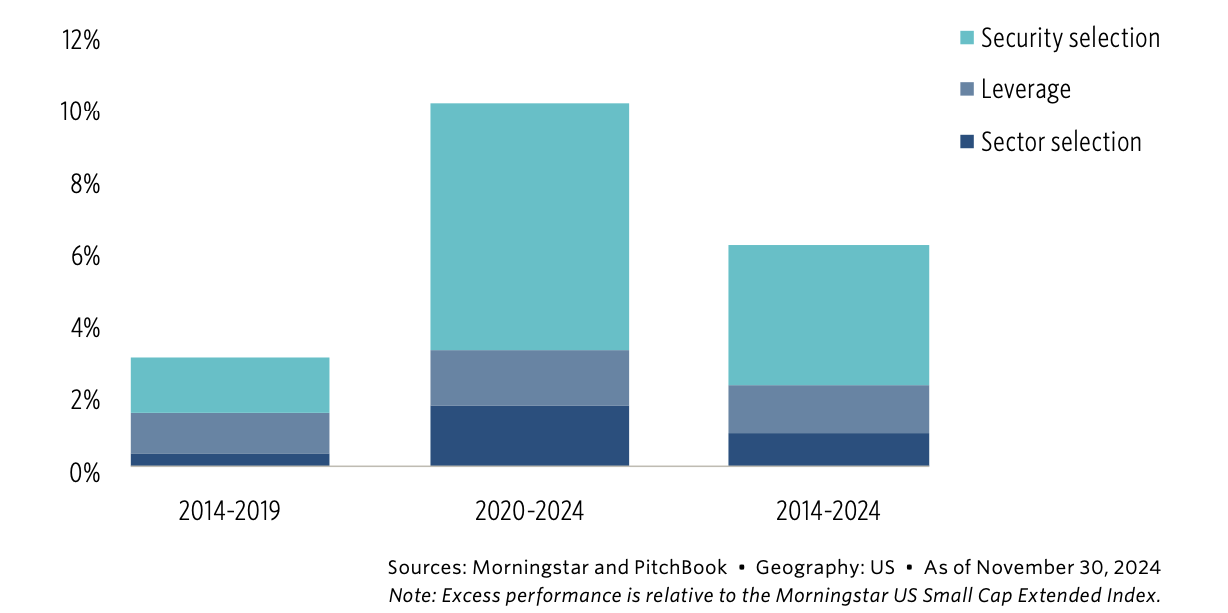

Morningstar PitchBook Buyout Replication Index excess performance attribution (annualized)

A returns-based factor analysis using the Fama-French five-factor model plus momentum reveals that the positive alpha from security selection can be explained primarily by a higher market beta.