Chart of the Week: Interesting Rates

Expectations for an improved economy has driven yields and time to a Fed hike in opposite directions.

Expectations for an improved economy has driven yields and time to a Fed hike in opposite directions.

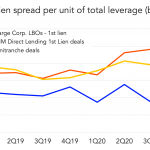

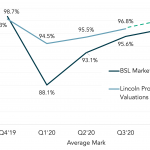

First-lien middle market direct lending deals proved the best value vs. large cap and unitranches.

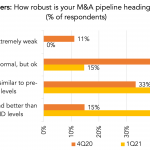

A “whopping” 85% of direct lenders characterized deal flow expectations as equal or better than pre-Covid levels.

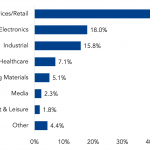

Reflecting investors’ preference for defensive sectors, business services led all industries for loans recently launched.

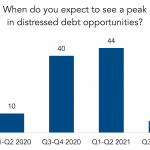

Most investors expect distressed loans to peak before the second half of 2021.

Over the past two decades business cycles have increased the degree of correlation among asset classes.

Leveraged loan prices recovered steadily through 2Q and 3Q 2020, bringing cumulative returns to positive territory.

Last year was Exhibit A on how non-traded loans perform amid volatility relative to their liquid cousins.

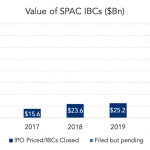

The value of initial business combinations (IBCs) produced by SPAC IPOs has reached unprecedented levels in 2020.

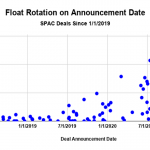

SPAC related IPOs are showing higher float rotation on the dates deals are announced.